Are capital gains considered earned income India?

Are investment income and capital gains taxed in India? If so, how? Income from the transfer of a capital asset situated in India is deemed to accrue in India. Hence, all individuals are liable for tax on capital gains arising from the transfer of capital assets in India.

What is the impact of an implication of long term capital gain taxation in India?

Tax Implications on LTCG on Property Currently, the long term capital gain tax rate on property is set at 20% with the addition of cess and surcharge. This tax rate is applicable on every property sold after 1st April 2017. However, this tax implication is not valid for any inherited property.

What is the tax on capital gains in India?

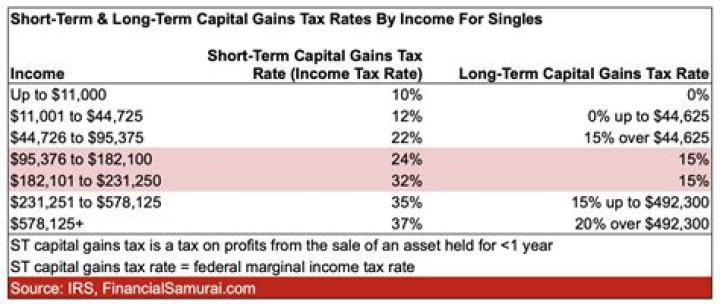

15%

Tax on Short-Term and Long-Term Capital Gains

| Tax Type | Condition | Tax applicable |

|---|---|---|

| Short-term capital gains tax | When securities transaction tax is applicable | 15%. |

Can a loss be set off against a capital gain?

However, short-term capital loss can be set off against long-term or short-term capital gain. 3) No loss can be set off against income from winnings from lotteries, crossword puzzles, race including horse race, card game, and any other game of any sort or from gambling or betting of any form or nature.

What’s the inclusion rate for capital gains for 2020?

Inclusion rate – generally, the inclusion rate for 2020 is 1/2. This means that you multiply your capital gain for the year by this rate to determine your taxable capital gain. This means that you multiply your capital gain for the year by this rate to determine your taxable capital gain.

What was long term capital gain under Income Tax Act 1961?

The Article Discusses about Tax Treatment of Long Term Capital Gain arising from Transfer of Capial Assets under Income Tax Act, 1961.

How to calculate recapture or terminal loss for capital gains?

Calculation of recapture or terminal loss based on 3 different selling prices Description A ($) B ($) C ($) Proceeds of disposition 4,000 8,000 12,000 Minus: Capital cost − 10,000 − 10,000 − 10,000 Capital gain = 0 = 0 = 2,000