Are loan fees considered intangible assets?

For tax purposes, intangible assets generally need to be amortized over a specified period of time, depending on the type of asset or life of the asset. Loan fees are amortized over the life of the loan. Intangible assets are generally shown in the other asset section of a balance sheet as one of the last items.

What is the amortization code for loan fees?

Loan fees and other amounts properly allocable to indebtedness can be amortized over the term of the loan notwithstanding IRC section 162(k).

What is an amortization fee?

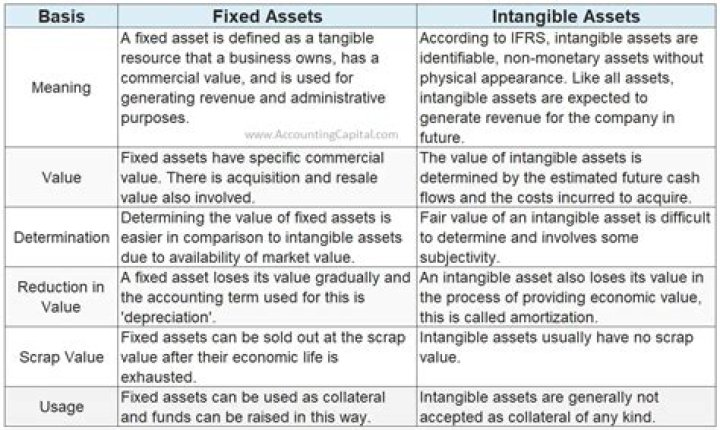

Amortized cost is that accumulated portion of the recorded cost of a fixed asset that has been charged to expense through either depreciation or amortization. Depreciation is used to ratably reduce the cost of a tangible fixed asset, and amortization is used to ratably reduce the cost of an intangible fixed asset.

What is included in amortization of intangibles?

The amortization of intangibles involves the consistent reduction in the recorded value of an intangible asset over its projected life. Amortization refers to the write-off of an asset over its expected period of use (useful life). Intangible assets do not have physical substance.

How is the amortization of intangibles determined?

A taxpayer shall be entitled to an amortization deduction with respect to any amortizable section 197 intangible. The amount of such deduction shall be determined by amortizing the adjusted basis (for purposes of determining gain) of such intangible ratably over the 15-year period beginning with the month in which such intangible was acquired.

Can you include intangibles in loan acquisition cost?

Loan acquisition cost is an expense, and accountants include its impact on the total loan amount. Businesses cannot include intangible assets as part of the loan acquisition costs.

Why is amortizable intangible not included in Section 197?

The term “amortizable section 197 intangible ” does not include any section 197 intangible acquired in a transaction, one of the principal purposes of which is to avoid the requirement of subsection (c) (1) that the intangible be acquired after the date of the enactment of this section or to avoid the provisions of subparagraph (A).

How are capitalized costs of intangible assets treated?

The INDOPCO regulations are capitalization provisions, not cost recovery provisions. For the latter, taxpayers should refer to: Sec. 167, 8 in which the cost of an intangible asset is: In some cases, amortized using the units-of-production method or the income-forecast method.