Are long term capital losses limited?

Can I deduct my capital losses? Any excess net capital loss can be carried over to subsequent years to be deducted against capital gains and against up to $3,000 of other kinds of income. If you use married filing separate filing status, however, the annual net capital loss deduction limit is only $1,500.

The IRS allows an individual or married taxpayer’s capital losses to be carried over for an unlimited number of years until the loss is exhausted. A capital loss that is carried over to a later tax year retains its long-term or short-term character for the year to which it is carried.

What counts as a capital loss?

A capital loss is the loss incurred when a capital asset, such as an investment or real estate, decreases in value. This loss is not realized until the asset is sold for a price that is lower than the original purchase price.

How much capital loss can I carry over to next year?

You’re limited to $3,000 per year in net capital losses that you can deduct from your other income, but this doesn’t mean that any losses over this amount are wasted. The remainder can be carried over to following years and can be applied to gains and income at that time. There’s no limit to the number of years you can do this.

Is there a limit to the number of years you can carry a loss forward?

There is no limit to the number of years you can carry a capital loss forward. However, you are not allowed to carry a capital loss backto a year before the capital loss occurred. The capital loss limitation is one of the most important facts of life in the tax world of an investor.

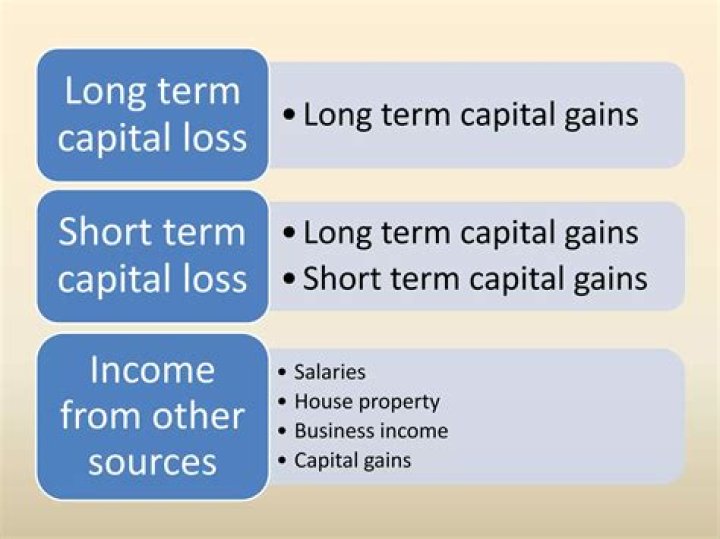

How are short term and long term capital losses treated?

“A short-term loss you carry over to the next tax year is added to short-term losses occurring in that year. A long-term loss you carry over to the next tax year is added to long-term losses occurring in that year. A long-term capital loss you carry over to the next year reduces that year’s long-term gains before its short-term gains.

How to claim net capital losses of prior years?

To use net capital losses of prior years to reduce current year taxable capital gains, claim a deduction on line 25300 of your income tax and benefit return. To carry a current year net capital loss back to 2017, 2018 or 2019, complete Form T1A , Request for Loss Carryback , and include it with your 2020 income tax and benefit return.