Can an employer match contributions to a 403 B?

No. An employer may, but is not required to, contribute to the 403(b) plan for employees. Q. What is the maximum annual combined amount the employer and employee can contribute to a 403(b) plan for an employee?

Can you retroactively contribute to 403b?

You may retroactively: adopt plan amendments that match the 403(b) plan to its prior operation, or. correct plan operation to match the 403(b) written plan terms.

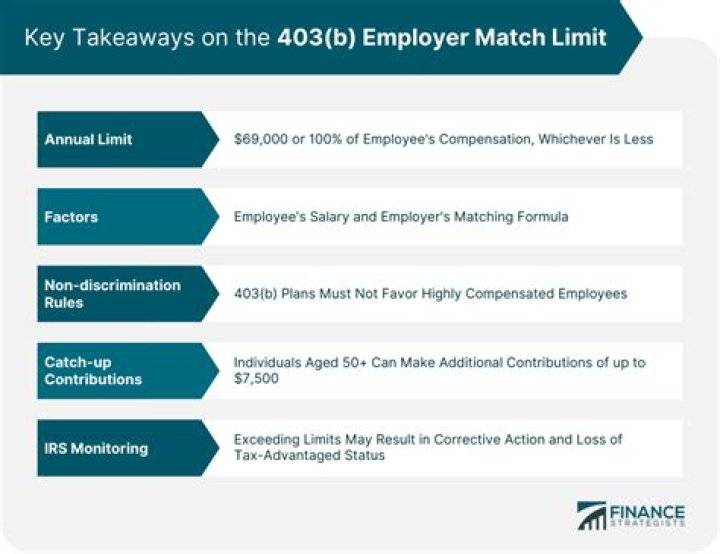

What is the max an employer can contribute to 403b?

$58,000

The limit on annual additions (the combination of all employer contributions and employee elective salary deferrals to all 403(b) accounts) generally is the lesser of: $58,000 for 2021 ($57,000 for 2020), or. 100% of includible compensation for the employee’s most recent year of service.

Under the RAP, the IRS will allow 403(b) plans to retroactively self-correct any defects in the form of the plan. Plans can be corrected for the period that starts on January 1, 2010 (or, if later, the effective date of the plan), and ends on March 31, 2020.

How much can my employer contribute to my 403 B?

What’s the maximum salary you can contribute to a 403B plan?

Basic salary deferral (the maximum payroll amount an employee can contribute to their 403 (b) plan by having money taken out of their check) is $19,500 as of 2021. 7 Employees 50 years and older can add $6,500 per year in special 403 (b) contributions called “catch-up” 403 (b) contributions.

Can a employer match an employee’s contribution to a 403B plan?

Employees can have their employers defer portions of their pay to these retirement accounts so that these earnings aren’t subject to income tax until the money is later withdrawn. Employers can match employees’ contributions.

Can a 50 year old contribute to a 403B plan?

Employees 50 years and older can add $6,500 per year in special 403 (b) contributions called “catch-up” 403 (b) contributions. This is in addition to the $19,500 that all employees can put aside. 7

What happens to your 403B plan when you change jobs?

Once you are vested in your 403 (b) plan, you can take the money with you when you change jobs. You will likely need to roll it over in an IRA account. 6 If you are not vested, you will lose your employer’s contributions, but you will keep the money that you have put into your retirement plan yourself.