Can an S Corp have a 105 plan?

Section 105 Eligibility: S-Corporation Owners S-Corporation (“S-Corp”) owners that own >2% of the company’s shares and their spouse, parents, children, and grandchildren, may use the Section 105 plan platform to track medical expenses, but will not receive reimbursements tax-free.

Can S Corp pay medical expenses?

You can get reimbursed for Medical Expenses! This is a major benefit of having reasonable compensation through your corporation. When you are an active shareholder with a W2 wage through the company you can get reimbursed for out of pocket expenses & medical insurance premiums!

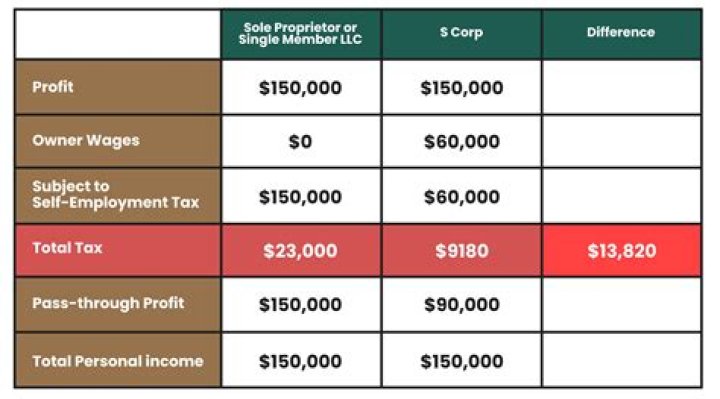

How are S-corp salaries calculated?

The IRS guidelines suggest you look at the following factors to determine reasonable salaries for your corporate officers:

- Training and experience.

- Duties and responsibilities.

- Time and effort devoted to the business.

- Dividend history.

- Payments to non-shareholder employees.

- Timing and manner of paying bonuses to key people.

What is a 105 reimbursement plan?

Section 105 of the Internal Revenue Service (IRS) regulations allows for reimbursement of medical expenses under an employer-sponsored health plan. There are various types of Section 105 plans including: Health Reimbursement Arrangements, Medical Expense Reimbursement Plans, Accident and Health Plans, and more.

How does COBRA work with HRA?

If an individual elects COBRA continuation coverage, an HRA complies with these COBRA requirements by providing for the continuation of the maximum reimbursement amount for an individual at the time of the COBRA qualifying event and by increasing that maximum amount at the same time and by the same increment that it is …

How are HRA COBRA premiums calculated?

Maximum single annual HRA reimbursement is $1,000. At 60% utilization the premium should be based on $600 ($1,000 x 60%). The monthly premium for the HRA component would be $50 ($600 ÷ 12 = 50). You (or your COBRA TPA) may add 2% to the premium for COBRA administration fees.

What is a Section 105 HRA?

Section 105 plans are a type of reimbursement health plan that allows small businesses to reimburse their employees for medical costs tax-free. As such, they’re a popular alternative to traditional group health insurance. Watch our on-demand webinar: how the HRA works for employers.

Is HRA considered income?

The account allows for employees to pay for eligible healthcare expenses. Unlike a Flexible Spending Account (FSA) or Health Savings Account (HSA), the employer owns the HRA and completely funds it; employees do not contribute and it does not count as taxable income.

Who is eligible for Section 105 base HRA?

BASE® HRA Plan Eligibility. The BASE® Health Reimbursement Arrangement is a great method of increasing tax savings for small business owners. A Section 105 BASE® HRA can be administered to a wide variety of small businesses, such as a farmer and rancher, self-employed computer contractor, and more.

What are IRS Section 105 and reimbursement plans?

HRAs in Zenefits. IRS Section 105 addresses the exclusion of reimbursements provided by an accident or health plan for the medical expenses of an individual or their dependents from the individual’s gross taxable income. An example of a Section 105 plan is a Health Reimbursement Account (HRA).

What is the carry forward amount for HRA 105?

With the Section 105 BASE ® HRA, an employee is able to carry forward unused benefit amounts to subsequent plan years up-to the maximum carry forward amount established by the employer at the onset of the plan administration.

Is the base HRA a tax savings plan?

The BASE ® HRA is an IRS-approved tax savings plan created through Code Section 105 of the Internal Revenue Code that allows business owners the opportunity to deduct these expenses as a business deduction. Around since 1954, this type of HRA was granted Safe Harbor in the Affordable Care Act (ACA) for businesses with 1 employee.