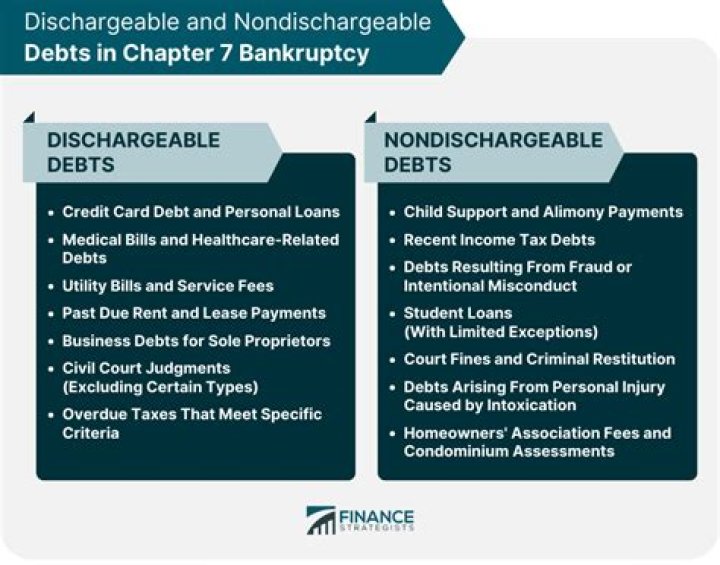

Can back taxes be discharged in Chapter 7?

Most tax debts won’t be wiped out by Chapter 7 bankruptcy, but some older tax obligations might. Typically, you can’t eliminate income tax liability by filing for Chapter 7 bankruptcy, but an exception exists.

You will be able to get rid of your tax debts in Chapter 7 bankruptcy if you meet the following requirements: The taxes are income-based. Income taxes are the only kind of debt that Chapter 7 is able to discharge. The tax debt must be for federal or state income taxes or taxes on gross receipts.

Can Chapter 13 Help With Back Taxes?

Instead, you repay your tax debts through the life of your Chapter 13 repayment plan, which could last either three or five years. But there are exceptions. Chapter 13 bankruptcy is an excellent tool to use when you fall behind on your taxes because it allows you to discharge (wipe out) old income tax debt.

When to include unpaid taxes in a bankruptcy?

The 2 year rule: failure to file your return on time. If you owe income taxes and did not file your tax return on time, then you cannot include those unpaid taxes in your bankruptcy case unless your tax return was filed at least two years before you filed your bankruptcy case.

What kind of tax return is filed during Chapter 7 bankruptcy?

During the chapter 7 or 11 bankruptcy, the debtor continues to file an individual tax return on Form 1040 or 1040-SR. The bankruptcy trustee files a Form 1041 for the bankruptcy estate.

How long does it take to file a bankruptcy tax return?

An automatic 6-month extension of time to file a bankruptcy estate income tax return is available for individuals in chapter 7 or chapter 11 bankruptcy proceedings upon filing a required application. Bankruptcy Code tax filing requirements.

Can a bankruptcy estate be carried back to a tax year?

If the administrative expenses of the bankruptcy estate are more than its gross income for a tax year, the excess amount may be carried back 3 years and forward 7 years. The amounts can only be carried to a tax year of the estate and never to a debtor’s tax year.