Can I take the mortgage interest deduction?

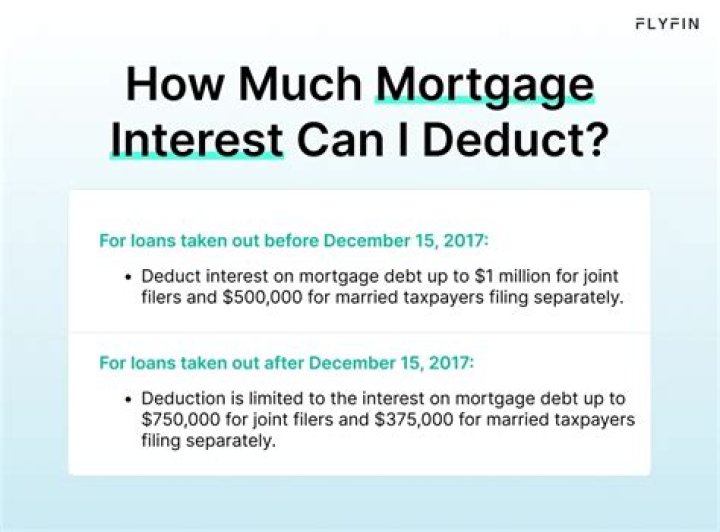

Mortgage Interest Deduction Limit Today, the limit is $750,000. That means this tax year, single filers and married couples filing jointly can deduct the interest on up to $750,000 for a mortgage if single, a joint filer or head of household, while married taxpayers filing separately can deduct up to $375,000 each.

That means this tax year, single filers and married couples filing jointly can deduct the interest on up to $750,000 for a mortgage if single, a joint filer or head of household, while married taxpayers filing separately can deduct up to $375,000 each. All of the interest you pay is fully deductible.

Is mortgage interest 100% deductible?

Many non-homeowners have very simple tax situations, so a primer on tax basics is in order. This deduction provides that up to 100 percent of the interest you pay on your mortgage is deductible from your gross income, along with the other deductions for which you are eligible, before your tax liability is calculated.

How do I calculate tax savings on mortgage interest?

If you itemize your deductions, you can deduct mortgage interest paid up to a certain amount. This deduction will reduce your taxes by whatever percentage represents your marginal tax rate. Calculating tax savings from mortgage interest will depend upon your tax bracket and how much interest you paid.

When do you get the mortgage interest deduction?

For the 2020-21 tax year, you could deduct one quarter of your mortgage interest payments, while three quarters of your mortgage interest payments received the tax credit. For previous years: In the 2017-18 tax year, you could claim 75% of your mortgage tax relief

Are there any tax savings in paying off a mortgage early?

This means that unless you have a special tax situation or a very expensive mortgage, the maximum tax savings a mortgage interest deduction in itself can provide are negligible. Paying off a mortgage early involves making monthly payments that are above the minimum amount due.

Is the interest on a second mortgage deductible?

Home equity loan tax deduction With a home equity loan, which is often referred to as a “second mortgage,” you receive a lump-sum payment based on your equity that will need to be paid back over the life of the loan. As with HELOCs, home equity loan interest is tax-deductible only if it’s used for buying, building, or renovating your home.