Can life insurance policies that build cash value be used to borrow money?

As cash value builds in a whole or universal life insurance policy, policyholders can borrow against the accumulated funds. Life insurance policy loans have one distinct advantage: The money goes to your bank account tax-free.

How much can I borrow from my life insurance policy Canada?

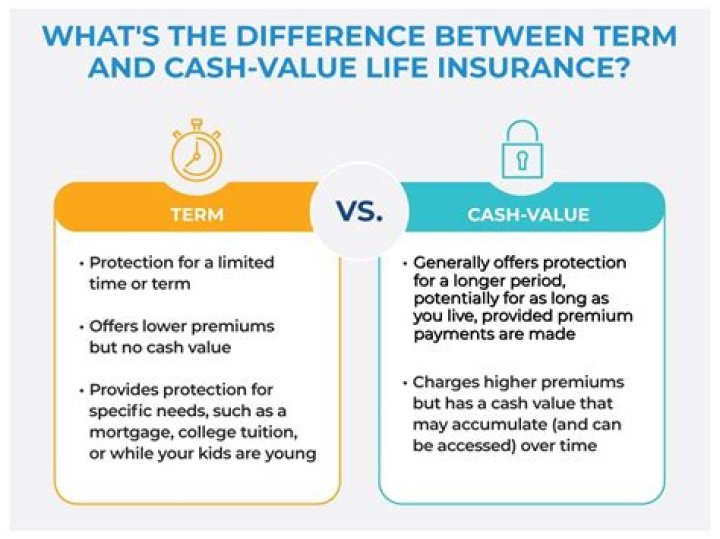

Term insurance policies don’t include cash value. This means you can’t borrow against your policy and you won’t get any cash value back if you cancel your policy. Some term policies can be renewed. Generally, your insurance company will establish your premiums, or the fees you pay, for the length of the term.

How can I borrow money from my life insurance policy?

Once the money invested increases the amount of the death benefit, the tax-free cash value can then be borrowed against. It is also important to understand that the policy loan is not taken out of your death benefit but borrowed against it, and the insurance company is using your policy as collateral for the loan.

What’s the difference between a loan and a life insurance policy?

One big difference between policy loans and traditional loans is that you don’t have to pay back the loan to your insurance policy. When you borrow based on your life insurance policy’s cash value, you are borrowing money from the life insurance company.

What happens if you fail to repay a life insurance loan?

A policy loan is issued by an insurance company and uses the cash value of a person’s life insurance policy as collateral. If a borrower fails to repay a policy loan, the money is withdrawn from the insurance death benefit.

How does a whole life insurance policy work?

Policy loans are borrowed against the death benefit, and the insurance company uses the policy as collateral for the loan. Insurance companies add interest to the balance, which accrues whether the loan is paid monthly or not. A whole life policy is more expensive but has no expiration date.