Can loss of discontinued business be carried forward?

Business losses can be carried forward and set off in the subsequent years even if the business has been discontinued. Losses from specified businesses that are allowed investment-linked deduction under Section 35AD of the Income Tax Act can be set off against gains from only the specified businesses.

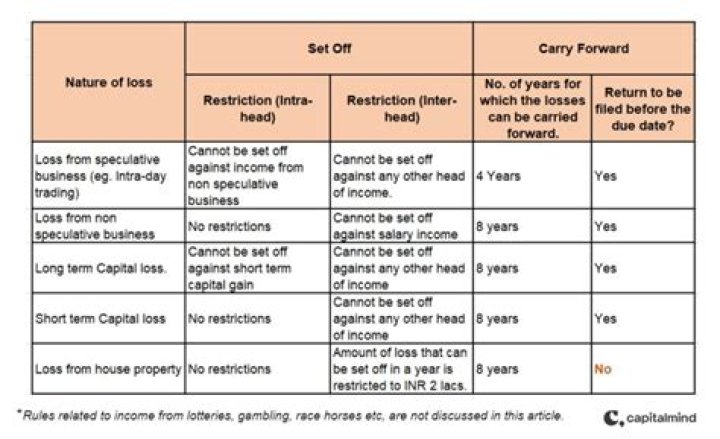

Can loss from house property be carried forward?

The total loss from house property can be adjusted with any other sources of income such as salary etc. Note that under the new ‘simplified’ tax regime, loss under the head ‘House Property’ cannot be set off against any other head of income and cannot be carried forward either.

How many years business loss can be carried forward?

eight years

Business loss can be carried forward for a period of eight years. However, each year’s loss must be treated as a separate loss. Though business loss can be carried forward for eight years only, the following types of expenses can be carried forward indefinitely: Unabsorbed depreciation.

Can business loss be set off against other income?

2) Loss from speculative business cannot be set off against any other income. However, non-speculative business loss can be set off against income from speculative business. 3) Loss under head “Capital gains” cannot be set off against income under other heads of income.

What is business loss carry forward?

A loss carryforward refers to an accounting technique that applies the current year’s net operating loss (NOL) to future years’ net income to reduce tax liability. This results in lower taxable income in positive NOI years, reducing the amount the company owes the government in taxes.

When does a loss carryforward expire for a business?

Loss Carryforward and the Internal Revenue Service. The Internal Revenue Service (IRS) allows businesses to carry net operating losses (NOL) forward 20 years. After that point, the losses expire and can no longer be used to reduce taxable income.

Can a business loss have a carryover effect?

Normally, a business loss reduces your other taxable income in the year that it occurred, and there is no carryover. But you could have a carryback/carryover if you had an actual Net Operating Loss (NOL ).

Can a business carry a net operating loss forward 20 years?

The Internal Revenue Service (IRS) allows businesses to carry net operating losses (NOL) forward 20 years. After that point, the losses expire and can no longer be used to reduce taxable income.

Can a business loss be carried forward to a future tax year?

If your business loss for the year is greater than the loss allowed for the year because it is over the excess loss limit, you may be able to carry forward the excess loss to a future tax year. See IRS Publication 536 about Net Operating Losses for more details. Let’s say Pam (a single taxpayer) had a business loss of $125,000 this tax year.