Can you borrow against home equity?

Home equity loans allow you to borrow against your home’s value, minus the amount of any outstanding mortgages on the property. Suppose your home is valued at $300,000, and your mortgage balance is $225,000. That’s $75,000 you can potentially borrow against.

How long can you borrow against a Heloc?

A HELOC has a credit limit and a specified borrowing period, which is typically 10 years. During that time, you can tap into your line of credit to withdraw money (up to your credit limit) when you need it. You use the funds only when you need to, and you can continue to use the funds as you repay them.

What happens if you have a home equity line of credit?

Home Equity Line of Credit (HELOC) A HELOC amounts to an open checkbook for people with equity in their home. However, there is a huge risk – foreclosing on your house – if you can’t repay the loan when it comes due.

What’s the difference between a home equity loan and a HELOC?

A home equity loan comes as a lump sum of cash, often with a fixed interest rate. Home equity lines of credit (HELOC) are a revolving source of potential funds, much like a credit card, that you use as you see fit with a variable interest rate. Banks underwrite second mortgages much like other home loans.

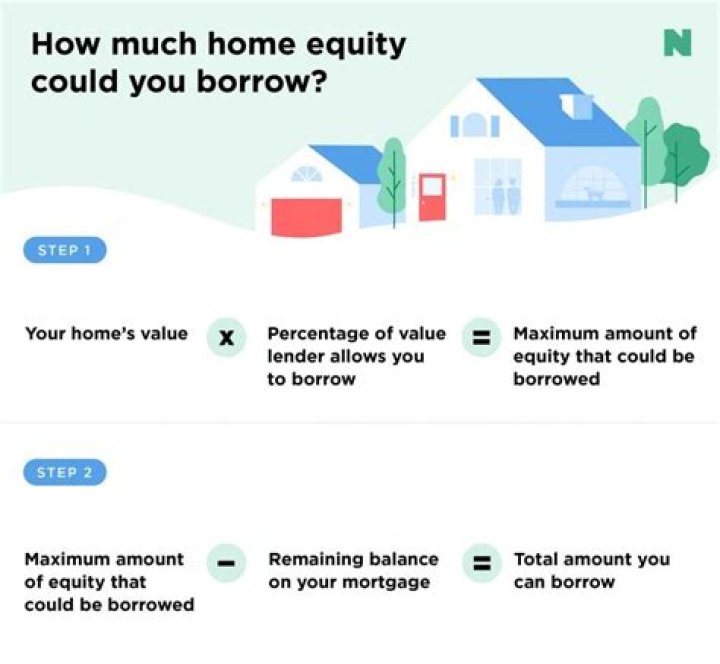

What’s the maximum amount you can borrow with a home equity line of credit?

The maximum amount of your home equity line of credit will vary based on the value of your home, what percentage of that value the lender will allow you to borrow against and how much you still owe on your mortgage. Two quick calculations can give you an idea of what you might be able to borrow with a HELOC.

Can a home equity loan be used as collateral?

Since a HELOC will use the home as collateral, it’s important to make sure the loan is worthwhile. Home equity loans offer borrowers a lump sum of capital that the bank will expect to be repaid over a predetermined period of time. A HELOC is a revolving line of credit that can be tapped into whenever the borrower likes.