Can you have an HSA without a medical plan?

Yes, you can open a health savings account (HSA) even if your employer doesn’t offer one. And you can’t be covered by other disqualifying coverage such as Medicare, Medicaid, TRICARE or a spouse’s health plan. Nor can you be claimed as a tax dependent in that year.

Can you have an HSA and a traditional plan?

If your spouse has a traditional health insurance plan, such as a PPO or HMO, that provides individual coverage only, then yes, you are eligible to participate in an HSA, but only if you are enrolled a high-deductible health plan and your spouse doesn’t also have a Healthcare FSA or HRA that covers your healthcare care …

What is the difference between HSA and regular health insurance?

An HSA is a tax-advantaged account established to pay for qualified medical expenses of an account holder who is covered under a high-deductible health plan. A HDHP is simply health insurance that meets certain minimum deductible and maximum out-of-pocket expense requirements.

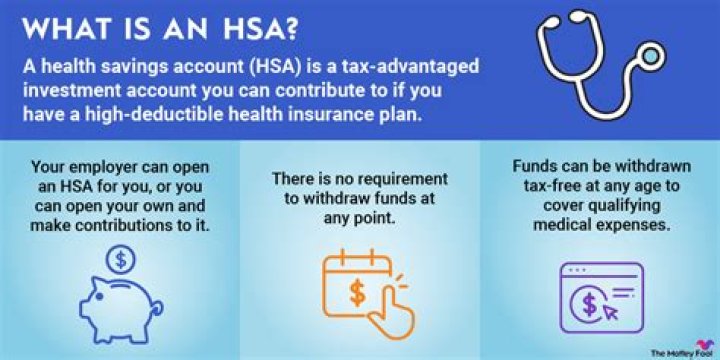

Is HSA connected to health insurance?

Health savings accounts (HSAs) are like personal savings accounts, but the money in them is used to pay for health care expenses. You — not your employer or insurance company — own and control the money in your HSA . One benefit of an HSA is that the money you deposit into the account is not taxed.

What happens if you contribute to HSA without HDHP?

No matter which way you go, remember you can’t make contributions once you no longer have a qualifying HDHP. The silver lining is that you own your HSA and have options on handling the funds when you are no longer HSA-eligible.

How do you know if a plan is HSA eligible?

For a health plan to be HSA-qualified, it must meet the following criteria for 2018: The minimum deductible must be no less than $1,350 for individual plans and $2,700 for families. No other health insurance besides an HDHP is allowed to qualify for an HSA, including Medicare.

Can I have an HSA without a high deductible plan?

While you can use the funds in an HSA at any time to pay for qualified medical expenses, you may contribute to an HSA only if you have a High Deductible Health Plan (HDHP) — generally a health plan (including a Marketplace plan) that only covers preventive services before the deductible.

What can HSA be spent on?

You can pay for a wide range of IRS-qualified medical expenses with your HSA, including many that aren’t typically covered by health insurance plans. This includes deductibles, co-insurance, prescriptions, dental and vision care, and more.

How much should I contribute to my HSA?

A guide to help you In 2021, the IRS allows individuals to contribute $3,600 to an HSA, and $7,200 for families. If you are over age 55 you can contribute an additional $1,000. If your employer is also contributing to your HSA, it counts toward this annual maximum. Your HSA can cover those costs.

Can I still have an HSA without a high deductible plan?

Generally, to be eligible to contribute to an HSA an individual cannot be covered by another health plan that is not an HDHP.

Is a high deductible HSA plan worth it?

HSA Basics HSAs have risen in popularity over the past few years because, in combination with high-deductible health plans (HDHPs), they can vastly reduce the monthly premium you and your employer pay. A higher deductible means lower premiums and that could mean huge savings for you and your employer.

What do you need to know about health savings accounts?

To be eligible to open an HSA, you must have a special type of health insurance called a high-deductible plan. Why were health savings accounts created? HSAs and high-deductible health plans were created as a way to help control health care costs.

What should I do with my HSA money?

Bookmark this page so you can always spend your HSA funds in the smartest way possible. Please note that this site is an educational reference only—not all health savings accounts are the same, and you should always check with your HSA administrator or health insurance provider to confirm if something is eligible before making a purchase.

Do you have to have health insurance to open an HSA?

You — not your employer or insurance company — own and control the money in your HSA. The money you deposit into the account is not taxed. To be eligible to open an HSA, you must have a special type of health insurance called a high-deductible plan. Why were health savings accounts created?

What’s the difference between a MSA and a health savings account?

A Health Savings Account (HSA) is an account for individuals with high-deductible health plans to save for medical expenses that those plans do not cover. A Medical Savings Account (MSA) was a forerunner of a Health Savings Account (HSA) and had similar deductibles, IRA status, and tax treatment.