Can you have bad debt on cash basis?

If you’re a cash method taxpayer (most individuals are), you generally can’t take a bad debt deduction for unpaid salaries, wages, rents, fees, interests, dividends, and similar items. For a bad debt, you must show that at the time of the transaction you intended to make a loan and not a gift.

Can I be cash-basis if I have inventory?

Inventory, including purchases and sales, must be treated on accrual-basis, but all other expenses and income may be considered under the cash method. If a business chooses to use the cash method for calculating income, however, then it must also use cash-basis for expenses.

Is loan write-off tax deductible?

The general rule is that where the debtor and creditor in a loan relationship are connected in any part of an accounting period and the whole or part of a loan is written off, then this is effectively a ‘tax nothing’, ie the creditor company cannot claim relief for the amount of the loan written off and the debtor …

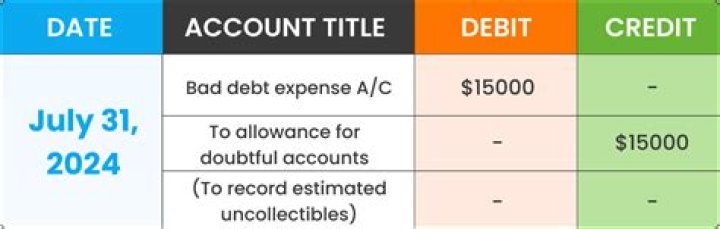

Can a taxpayer write off income on a cash basis?

Cash basis taxpayers have never picked up the income so therefore would not be allowed to write it off. However, the taxpayer can and has already deducted expenses associated with that customer.

How are expenses reported on a cash basis?

Cash basis reporting means that you report your income and expenses when they are received and paid respectively. Income is reported once the cash is received from the customer. Expenses are reported when paid (via check, credit card, or cash). Most small businesses report under the cash basis reporting method.

When do you have to declare cash basis?

This is because you only need to declare money when it comes in and out of your business. At the end of the tax year, you won’t have to pay Income Tax on money you didn’t receive in your accounting period. Cash basis probably won’t suit you if you: run a business that’s more complex, for example you have high levels of stock

What’s the difference between cash basis and accrual basis?

When reporting for your taxes there are two types of accounting methods: cash basis and accrual basis. Let’s take a brief look at each and then answer that question. This basis of accounting means that income and expenses are recognized when they accrue. Income is reported when the work is completed.