Can you write of mortgage interest in 2020?

The 2020 mortgage interest deduction Mortgage interest is still deductible, but with a few caveats: Taxpayers can deduct mortgage interest on up to $750,000 in principal. Home equity debt that was incurred for any other reason than making improvements to your home is not eligible for the deduction.

What is mortgage interest relief?

Mortgage Interest Relief is a tax relief on the interest you pay in a tax year on a qualifying mortgage loan. You can claim Mortgage Interest Relief on interest paid by you on a loan used to purchase, repair, develop or improve the home.

Can I claim my mortgage interest on taxes?

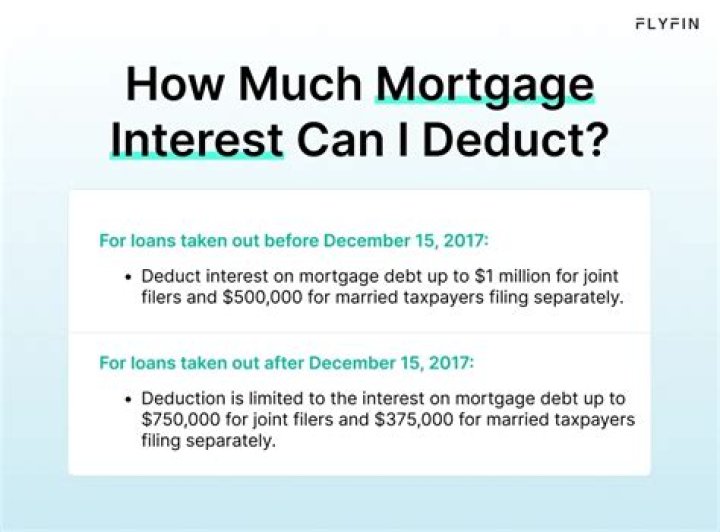

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible.

Are there any changes to the mortgage interest deduction?

Owning your own home comes with some nice tax perks. One of them is the home mortgage interest deduction. The Tax Cuts and Jobs Act (TCJA) affected this deduction somewhat when it went into effect in 2018, but the legislation did not eliminate the deduction from the tax code entirely. 1 It just sets some limits and restrictions.

Can You claim mortgage interest on a second home?

Only one second home may be used to claim the deduction. However, how you use the home will determine whether you can claim interest on its mortgage. If you don’t rent out the second home, then it counts as a qualified home even if you don’t live there during the year.

Can you deduct mortgage interest on a joint tax return?

You Must Be the Obligor The mortgage can’t be in someone else’s name unless it’s your spouse and you’re filing a joint tax return. You’re entitled to deduct only the mortgage interest that you personally paid, regardless of who received the Form 1098 from the lender. You must also have a contractual obligation to pay the loan back.

What’s the maximum amount of interest you can claim on a mortgage?

Together, the loans add up to $1.2 million, exceeding the $750,000 limit under the terms of the TCJA. You can only claim a mortgage interest deduction for the percentage attributable to the first $750,000 you borrowed. Interest associated with that other $450,000 is just money that you spent. You don’t get a tax break for it.