Do non-qualified annuities have 10 penalties?

Both qualified and non-qualified annuities require you to be 59 ½ before withdrawing funds. If you withdraw the money before that, the IRS imposes a 10-percent tax penalty on earnings. There are no federal legal requirements for when withdrawal must begin from non-qualified annuities.

Is there a 10% penalty on annuities?

Withdrawing money from an annuity can result in penalties, including a 10 percent penalty for taking funds from your annuity before age 59 ½. Alternatively, you can sell a number of payments or a lump-sum dollar amount of the annuity’s value for immediate cash.

What’s the penalty for withdrawing from a non qualified annuity?

Penalty. Non-qualified annuities fall under the same IRS rules governing traditional IRAs and other types of retirement plans when it comes to premature distributions. The penalty is 10 percent on the earnings portion plus regular income tax if you withdraw before you’re 59 1/2. If the value is equal to or below its original cost,…

How old do you have to be to take a non-qualified annuity?

Both qualified and non-qualified annuities require you to be 59 ½ before withdrawing funds. If you withdraw the money before that, the IRS imposes a 10-percent tax penalty on earnings.

Are there any non qualified annuity tax exceptions?

Other non-qualified annuity exceptions are for distribution which are either: Allocable to the cost or basis portion of a deferred annuity contract issued before August 14, 1982 Paid from an annuity contract under a qualified personal injury settlement (so called “structured settlement”)

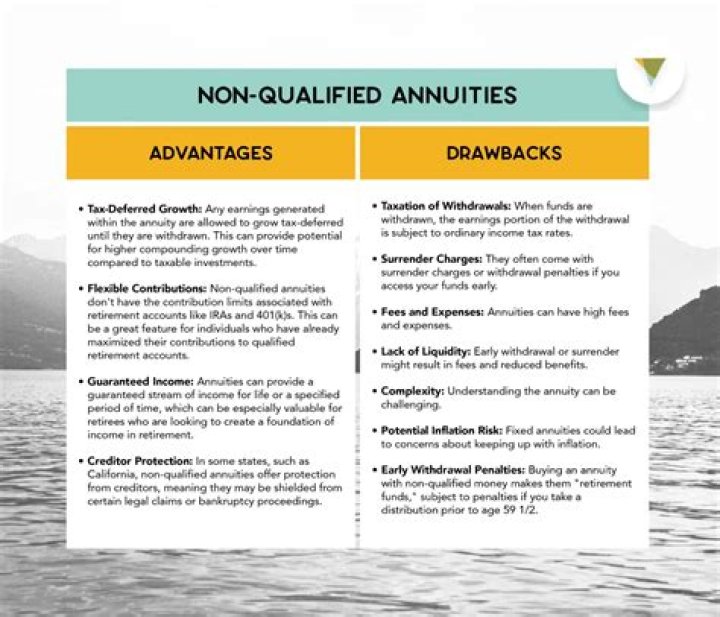

What are the pros and cons of non qualified annuities?

The fact that the IRS largely treats non-qualified annuities in a similar manner to tax-favored retirement accounts has some pros and cons. The biggest benefit of an annuity is that your investment can grow on a tax-deferred basis.