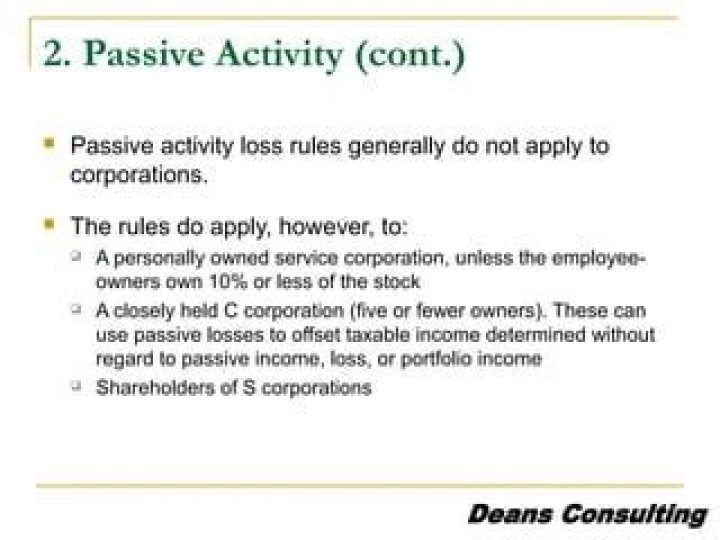

Do passive activity rules apply to corporations?

The passive activity rules apply to:

- Individuals,

- Estates,

- Trusts (other than grantor trusts),

- Personal service corporations, and.

- Closely held corporations.

Who do passive activity loss rules apply to?

Key Takeaways

- Passive activity loss rules are a set of IRS rules stating that passive losses can be used only to offset passive income.

- A passive activity is one wherein the taxpayer did not materially participate in its ongoing operation during the year in question.

Do passive activity loss rules apply to C corporations?

FREE – Guide to Real Estate Taxes The general rule is that income derived from real estate activity is passive and is subject to the Passive Activity Loss Limits. This is the general rule unless you or your closely held C corporation (C corp) qualifies as a real estate professional.

What are the property tax implications of dissolving an LLC?

Property Tax Implications of Dissolving an LLC Depending on a variety of factors, the IRS could say that you owned the home for eight out of 10 years as a rental property, the IRS may claim that you owe tax on 80 percent of the profits and could use the home sale exclusion for the other 20 percent.

Can a rental company be a S corporation?

However, if you own rental real estate, then you may want to consider forming a different entity. Here’s why. Holding real estate in an S corp does not pose a problem while it is held. You can collect rent, pay expenses, and put the property in the name of the S corporation.

How are assets distributed in a dissolvng Corporation?

For example, it is a common practice for corporations to sell the corporation’s assets upon dissolution and disburse the remaining assets to the shareholders after all prior liabilities are taken care of. As said, assets ‘distributed’ to the S/H are actually sold at fmv, and gain is recognized in the corp, which will pass thru on the K1.

What happens if you own real estate in a S corporation?

Holding real estate in an S corp does not pose a problem while it is held. You can collect rent, pay expenses, and put the property in the name of the S corporation. Business is run as usual, and asset protection is in effect if you operate the corporation property. The issues arise when it’s time to get the property out of the entity.