Do you need a profit and loss statement for self employed?

The IRS requires sole proprietors to use Profit or Loss From Business (Sole Proprietorship) (Schedule C (Form 1040)), to report either income or loss from their businesses.

How do you certify a profit and loss statement?

You need to hire a certified public accountant to provide a certified income statement. The CPA certifies financial statements by going over them, comparing them to reality, and certifying that the depiction of your finances is accurate.

Is profit/loss statement an income statement?

Profit and Loss (P&L) Statement A P&L statement, often referred to as the income statement, is a financial statement that summarizes the revenues, costs, and expenses incurred during a specific period of time, usually a fiscal year or quarter.

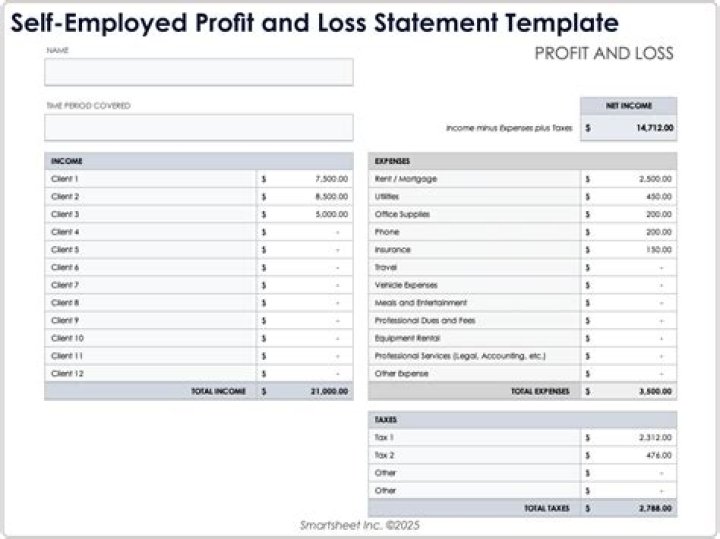

What is a Self Employment profit and loss statement?

The IRS self-employed year-to-date profit and loss statement requirements are reported in Form 1040–Schedule C Profit or Loss from Business. On this statement, you need to report your gross income from self-employment and your gross expenses.

Is there a difference between a P&L and an income statement?

P&L is short for profit and loss statement. A business profit and loss statement shows you how much money your business earned and lost within a period of time. There is no difference between income statement and profit and loss. An income statement is often referred to as a P&L.

What is included in profit and loss statement?

A Profit and Loss (P & L) statement measures a company’s sales and expenses during a specified period of time. The categories include net sales, costs of goods sold, gross margin, selling and administrative expense (or operating expense), and net profit.

How do I create a profit and loss account from my bank statement?

How to write a profit and loss statement

- Step 1: Calculate revenue.

- Step 2: Calculate cost of goods sold.

- Step 3: Subtract cost of goods sold from revenue to determine gross profit.

- Step 4: Calculate operating expenses.

- Step 5: Subtract operating expenses from gross profit to obtain operating profit.