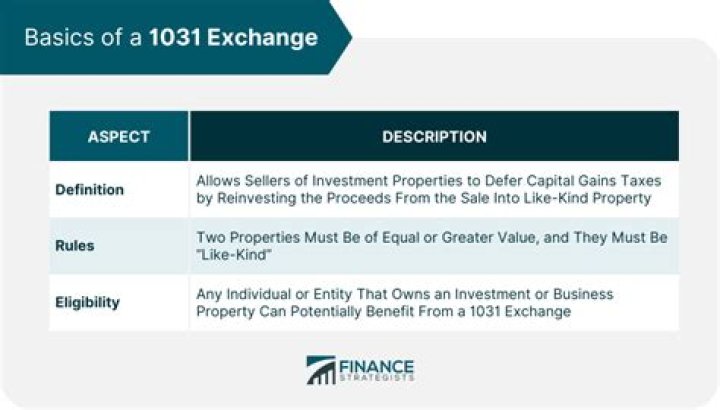

Does a 1031 exchange eliminate depreciation recapture?

1031 Exchanges allow you to defer both the capital gains tax and depreciation recapture from the sale of a property and invest the proceeds into another “like-kind” property, often called “trading up.”

How do you depreciate like kind exchange property?

Option 1: Generally, taxpayers must depreciate the carryover basis of property acquired in a like-kind exchange during the current tax year over the remaining recovery period of the property exchanged. They must use the same depreciation method and convention that was used for the relinquished property.

How does the 1031replacement property depreciation schedule work?

1031.us To develop the replacement property depreciation schedules, the Temporary Regulations split the new total basis of the replacement property between the “exchanged basis” and the “excess basis.” The exchanged basis is the remaining basis carried over from the relinquished property.

What happens to property received in a 1031 exchange?

If your heirs inherit property received through a 1031 exchange, its value is “stepped up” to fair market, which wipes out the tax deferment debt. This means that if you die without having sold the property obtained through a 1031 exchange]

Can a partnership be used in a 1031 exchange?

Interest in a partnership cannot be used in a 1031 exchange—partners in an LLC do not own property, they own interest in a property-owning entity, which is the taxpayer for the property. 1031 exchanges are carried out by a single taxpayer as one side of the transaction.

What is the new basis for 1031 Reinvestment?

If the taxpayer meets the 1031 reinvestment requirements and purchases replacement property of say $1.2 million, the total new basis for the replacement property received would be $630,000. This total new basis is computed by taking the $1.2 million cost of the new property and subtracting the $570,000 of gain deferred in the exchange.