Does a simple trust distribute income?

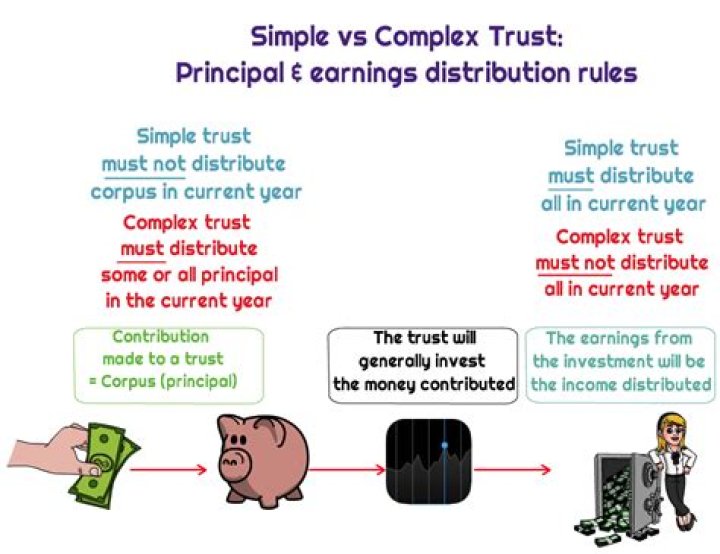

By definition, a simple trust is a trust: That requires all income must be distributed currently. That doesn’t provide any amounts to be paid, permanently set aside, or used for charitable purposes. That doesn’t distribute amounts allocated to the corpus of the trust.

How are beneficiaries of simple Trusts taxed?

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust’s income, rather than the trust itself paying the tax. However, such beneficiaries are not subject to taxes on distributions from the trust’s principal.

Can a simple trust not distribute income?

A simple trust must distribute all its income currently. Generally, it cannot accumulate income, distribute out of corpus, or pay money for charitable purposes. If a trust distributes corpus during a year, as in the year it terminates, the trust becomes a complex trust for that year.

Can a simple trust distribute principal?

Definition of a Simple Trust There are three basic characteristics that define a simple trust: The trust must annually distribute to the beneficiaries any income it earns on trust assets. The trust cannot distribute the principal of the trust. The trust cannot make distributions to charitable organizations.

What do you need to know about 1041 tax return?

About Form 1041, U.S. Income Tax Return for Estates and Trusts. The fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust.

How does an irrevocable trust report income to the IRS?

An irrevocable trust reports income on Form 1041, the IRS’s trust and estate tax return. Even if a trust is a separate taxpayer, it may not have to pay taxes. If it makes distributions to a beneficiary, the trust will take a distribution deduction on its tax return and the beneficiary will receive IRS Schedule K-1.

How is distributable net income taxed in a trust?

Distributable net income (DNI) is the amount of income that will be taxed to the beneficiary. Distributions in excess of DNI are treated as tax-exempt income or as principal and are not taxable to the beneficiary.

What do you need to know about a simple trust?

Simple Trust: The beneficiary of a simple trust must include in his or her gross income the amount of the income required to be distributed currently (as entered on Schedule B of Form 1041), whether or not distributed.