Does New York State have a corporate income tax?

Corporate income tax Tax rate increase for taxpayers with New York State income over $5 million For taxable years beginning in 2021, 2022, and 2023, the New York State corporate income tax rate imposed on the New York State business income base increases from 6.5% to 7.25% for any taxpayer with New York State …

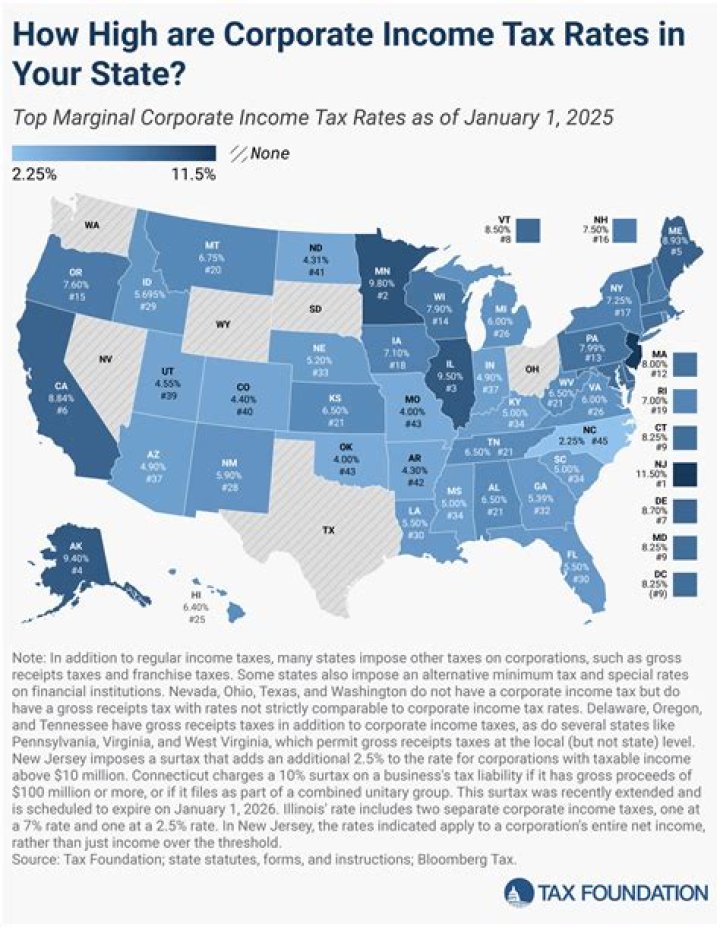

How much is corporate tax in NY?

Corporate tax rates – Part HHH. The legislation increases the corporate franchise tax rate to 7.25% from 6.5% for tax years beginning on or after January 1, 2021 and before January 1, 2024 for taxpayers with a business income base greater than $5 million.

New York has a corporation franchise tax, which applies to both traditional (C-type) corporations and to S corporations, and a tax known simply as the filing fee, which applies to LLCs, limited liability partnerships (LLPs), and some regular partnerships.

How much is NY state corporate tax?

The legislation increases the corporate franchise tax rate to 7.25% from 6.5% for tax years beginning on or after January 1, 2021 and before January 1, 2024 for taxpayers with a business income base greater than $5 million.

How are corporate taxes calculated in New York?

Corporate taxpayers in New York State pay tax equal to the highest amount calculated under three alternative tax bases: fixed dollar amount. The starting point for the New York State business income is the federal income tax base. Certain additions are required, including:

Do you have to file corporation tax in New York?

If your business is incorporated in New York State or does business or participates in certain other activities in New York State, you may have to file an annual New York State corporation tax return to pay a franchise tax under the New York State Tax Law. The way you compute the tax and the type of return you file will depend on…

What kind of tax do you pay in New York?

The S corporation’s nonresident shareholders pay New York tax —at the personal income tax rates—on just 10% of their share of the company’s income (assuming the corporation is taxed on its business income base) because only 10% of the receipts are New York source, and single-factor receipts-only apportionment is used.

When is a New York corporation required to pay a first installment?

A New York S corporation or continuing §186 corporation whose tax for the preceding tax year exceeded $1,000 is required to pay a mandatory first installment (MFI) with its tax return for the previous year or with the request for an extension of time to file such return.