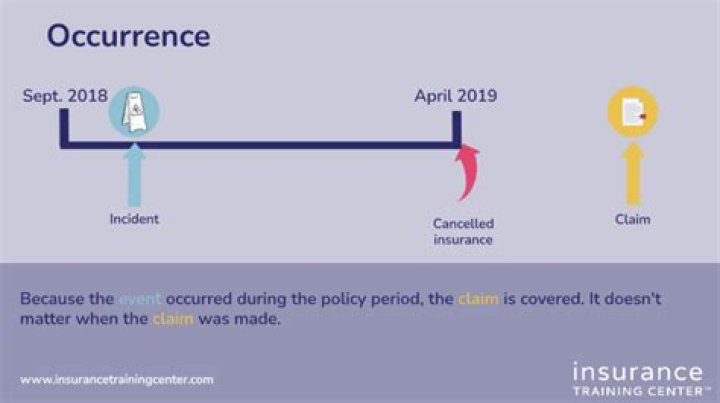

Does occurrence malpractice require a tail?

Occurrence Coverage The occurrence malpractice insurance policy will apply to all claims that occur during the time that you had the insurance coverage. It is not necessary for you to purchase any tail insurance, as any wrongful acts that occurred within the time that you had the policy will be eligible.

Is malpractice tail insurance tax deductible?

Yes, malpractice insurance, including tail, is tax deductible. For independent contractors and practice owners, it is a business expense. For employed doctors, it would be considered a job-related expense that can be listed under itemized expenses on Schedule A of Form 1040.

What is tail malpractice?

Tail malpractice coverage provides insurance coverage for claims brought after a claims-made insurance policy is terminated. This means there is no coverage for a claim brought after a claims-made policy is cancelled or not renewed. Tail malpractice coverage solves this problem.

What percent of malpractice suits are won?

Medical Malpractice Case Outcomes: Facts & Statistics According to their findings, physicians win 80% to 90% of jury trials with weak evidence of medical negligence, approximately 70% of borderline cases, and 50% of cases with strong evidence of medical negligence.

Why is claims-made better than occurrence?

In short, occurrence-based policies provide ample coverage as long as you keep renewing them. For this privilege, you’ll generally pay more than you would for claims-made policies. With claims-made policies, the amount of coverage you purchase must last for as long as you keep your policy.

How do you tell if an insurance policy is claims-made or occurrence?

An occurrence policy has lifetime coverage for the incidents that occur during its policy period, regardless of when the claim is reported. A claims-made policy only covers incidents that happen and are reported within the policy’s time frame, unless a ‘tail’ extension is purchased.

What is tail coverage malpractice insurance?

Which is better claims made or occurrence?

Occurrence Example An occurrence policy is typically more expensive than claims-made policy because there isn’t a limit on the time a claim must be reported. There’s no advantage to having a claims-made coverage over occurrence coverage, and vice versa.

What is the difference between claims made and occurrence malpractice?

An occurrence policy provides coverage for alleged incidents (injuries) that happened during the policy year regardless of when the claim is reported to the carrier. The renewed claims made policy covers claims that come in during the policy year for incidents that occurred on or after the retroactive date.

When does medical malpractice tail coverage go into effect?

In contrast to a standard policy, tail coverage provides protection for medical malpractice claims that are reported after the provider’s policy expired or was cancelled. Here is an example of how tail coverage works: Doctor A’s insurance policy is in effect from January 1, 2010 through December 31, 2020.

Do you have to deduct malpractice insurance on taxes?

According to the IRS, deductible insurance premiums include malpractice insurance that covers your personal liability for professional negligence resulting in injury or damage to patients or clients. For more information on IRS rules for deductible insurance, please see this link.

What’s the difference between nose and tail insurance?

Another option in lieu of tail coverage is “nose coverage.” Nose coverage is coverage for prior acts. It is offered by the doctor’s new or subsequent insurance policy to cover acts that occurred before the new policy took effect. It is basically the opposite of tail insurance, but effectively provides the same kind of coverage.

When is a medical malpractice claim is made?

When a medical malpractice claim is made after the health care provider’s insurance coverage has expired. Please answer a few questions to help us match you with attorneys in your area.