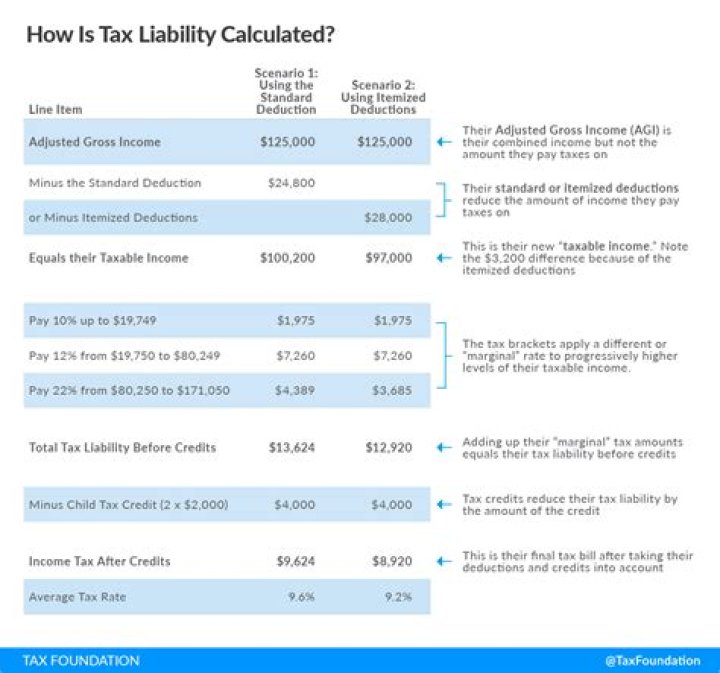

How are corporate tax liabilities calculated?

Your taxable income minus your tax deductions equals your gross tax liability. Gross tax liability minus any tax credits you’re eligible for equals your total income tax liability.

Is contingent liability a current liability?

Current and contingent liabilities are both important financial matters for a business. The primary difference between the two is that a current liability is an amount that you already owe, whereas a contingent liability refers to an amount that you could potentially owe depending on how certain events transpire.

Is deferred tax liability an asset?

Items on a company’s balance sheet that may be used to reduce taxable income in the future are called deferred tax assets. Therefore, overpayment is considered an asset to the company. A deferred tax asset is the opposite of a deferred tax liability, which can increase the amount of income tax owed by a company.

How to calculate deferred tax liability for income taxes?

Calculation of Deferred Tax Liability. Income Tax Expense= taxes payable + DTL – DTA. Deferred Tax Liability Formula = Income Tax Expense – Taxes Payable + Deferred Tax Assets. Year 1 – DTL = $350 – $300 + 0 = $50. Year 2 – DTL = $350 – $300 + 0 = $50.

Why does a company have a growing deferred tax liability?

For example, a growing deferred tax liability could signal that a company is capital intensive. This is because the purchase of new capital assets often comes with accelerated tax depreciation that is larger than the decelerating depreciation of older assets. Thank you for reading this guide to tax liabilities and assets.

Why do I have a deferred tax asset?

Any asset that has a higher book value is generally cause of a deferred tax. There can be other causes and you should know them well. A deferred tax is the difference between net income and income before taxes. For example if a company has $100 net income and $70 as taxable income, the deferred tax liability is $30. You can change a tax asset .

Is the timing difference of 50 a deferred tax liability?

The temporary timing difference of 50 is a tax liability which will need to be paid in the future as the timing differences reverse (see years 3 and 4 below). The movement of 50 is accounted for as a deferred tax liability with the following journal entry.