How are lump sum payments calculated?

The formula to calculate compound interest for a lump sum is A = P (1+r/n)^nt where A is future value, P is present value or principal amount, r is the interest rate, t is the number of years the money is deposited for and n is the number of periods the interest is compounded each year.

What is a lump sum payment Centrelink?

A lump sum is a one off amount of money. Lump sums can count in your income test. If so, they may affect your payment from us.

Do parents get citizenship through birth of their child in Australia?

Where one or both parents are Australian citizens or a permanent residents, the child automatically acquires Australian citizenship. As soon as the baby is born, the parents may apply for an Australian passport in respect of the child.

How long do you need to live in Australia to become a citizen?

To be eligible to apply for Australian citizenship, you must have: Been an Australian permanent resident for at least 1 year and lived in Australia for at least 9 out of 12 months before you apply. Been lawfully resident in Australia for at least 4 years before you apply.

Where can I get a lump sum payment?

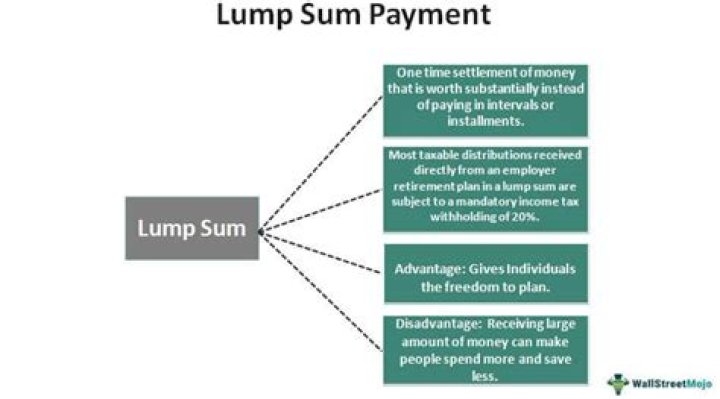

They are sometimes associated with pension plans and other retirement vehicles, such as 401k accounts, where retirees accept a smaller upfront lump-sum payment rather than a larger sum paid out over time. These are often paid out in the event of debentures .

Is it better to take a lump sum or a cash out?

A lump-sum payment may seem attractive. You give up the right to receive future monthly benefit payments in exchange for a cash-out payment now—typically, the actuarial net present value of your age-65 benefit, discounted to today. Taking the money up front gives you flexibility.

What are excluded from a lump sum payment?

Other things are considered income but are excluded in determining your monthly income.

When do you have to pay taxes on a lump sum?

Information For… If you were born before January 2, 1936, and you receive a lump-sum distribution from a qualified retirement plan or a qualified retirement annuity, you may be able to elect optional methods of figuring the tax on the distribution. These optional methods can be elected only once after 1986 for any eligible plan participant.