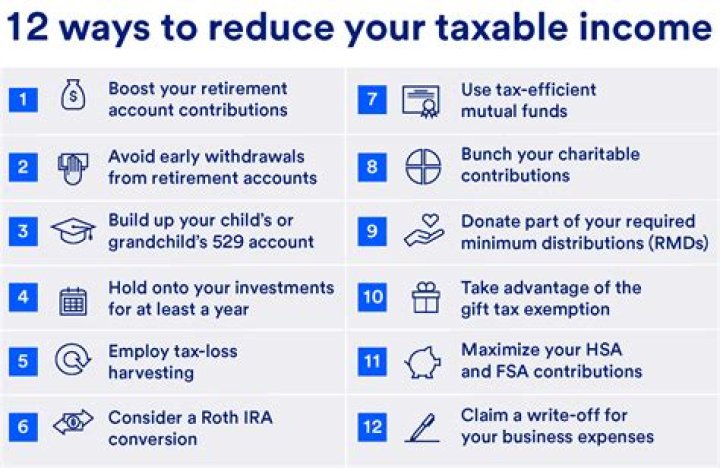

How can I lower my tax liability legally?

As of right now, here are 15 ways to reduce how much you owe for the 2020 tax year:

- Contribute to a Retirement Account.

- Open a Health Savings Account.

- Use Your Side Hustle to Claim Business Deductions.

- Claim a Home Office Deduction.

- Write Off Business Travel Expenses, Even While on Vacation.

What is the tax rate for $250000?

2019 Tax Rate Schedule 2019 Tax Rate Schedule

| Taxable Income1 | Federal Tax Rates | |

|---|---|---|

| Married Filing Joint | Single Filers | Income |

| $78,951 – $168,400 | $39,476 – $84,200 | 22% |

| $168,401 – $250,000 | $84,201 – $160,725 | 24% |

| – | $160,726 – $200,000 | 32% |

How can high income earners reduce tax liability?

Invest in tax-efficient index mutual funds and exchange-traded funds (ETFs). Every high-income earner should have a plan to diversify the taxation of income in retirement. For taxable accounts, a tax-efficient index mutual fund and/or ETF may help reduce the taxes you pay on your investments year-to-year.

How do I determine my tax liability limit?

Your taxable income minus your tax deductions equals your gross tax liability. Gross tax liability minus any tax credits you’re eligible for equals your total income tax liability.

How can I avoid higher tax bracket?

Consider these five ways to avoid spiking into a higher tax bracket this year:

- Contribute to retirement plans.

- Avoid selling too many assets in one year.

- Plan the timing of income and business expenses.

- Pay deductible expenses and make contributions in high-income years.

- If you’re a farmer or fisherman, use income averaging.

How do I limit my taxable income?

The simplest way to reduce taxable income is to maximize retirement savings. Those whose company offers an employer-sponsored plan, such as a 401(k) or 403(b), can make pretax contributions up to a maximum of $19,500 in 2021 (also $19,500 in 2020).

How can I reduce my income tax liability?

If you sell an investment that has lost value, you can use that loss to offset other income. The income tax you pay each year is based on your gross income, and for many of us, the easiest way to reduce that figure is by contributing to an employer-sponsored retirement plan or individually held traditional IRA.

How does incorporating reduce your liability and taxes?

Almost without fail, the doctor overestimates the decrease in liability and taxes to be paid, especially once the costs of incorporation are taken into account. We’ll try to set the record straight here. Incorporating doesn’t decrease your malpractice liability one iota.

Are there any below line deductions that will lower your taxes?

Unfortunately, not all below the line deductions will lower your taxable income. According to estimates, nearly 90% of taxpayers will end up taking the standard deduction rather than itemizing deductions.

What kind of tax do you pay on$ 200, 000 in income?

Like the federal income tax, FICA tax – the tax assessed on your income to cover contributions to Social Security and Medicare – apply no matter which state you live in. To keep things simple, we’re going to assume that the $200,000 income is being earned roughly equally by each spouse.