How do I get the most tax write offs?

Claim them if you deserve them, and keep more money in your pocket.

- State sales taxes.

- Reinvested dividends.

- Out-of-pocket charitable contributions.

- Student loan interest paid by you or someone else.

- Moving expenses to take your first job.

- Child and Dependent Care Tax Credit.

What if write offs are more than income?

If your deductions exceed income earned and you had tax withheld from your paycheck, you might be entitled to a refund. You may also be able to claim a net operating loss (NOLs). You can use your Net Operating Loss by deducting it from your income in another tax year.

How do billionaires save taxes?

In such cases, though, the data obtained by ProPublica shows billionaires have a palette of tax-avoidance options to offset their gains using credits, deductions (which can include charitable donations) or losses to lower or even zero out their tax bills.

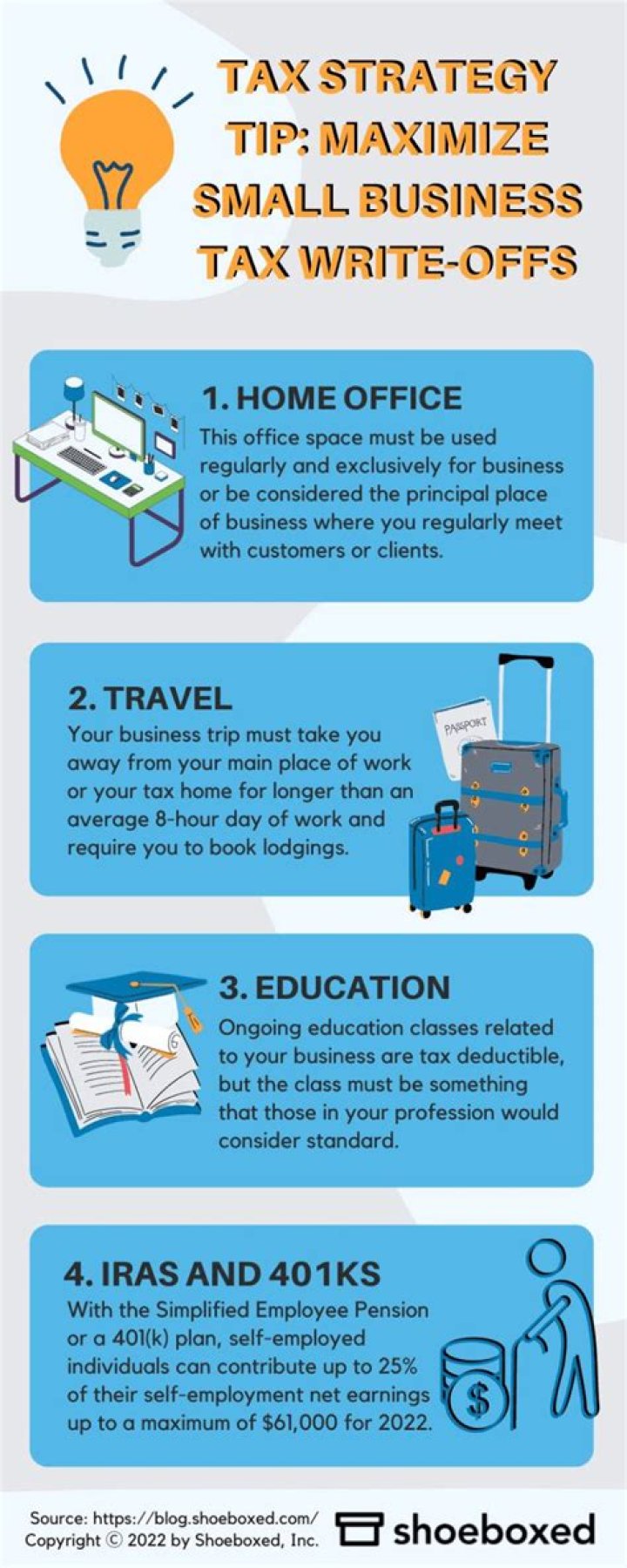

What is a write off for a small business?

A write-off is an expense that can be claimed as a tax deduction. Tax write-offs are deducted from total revenue to determine total taxable income for a small business. Qualifying write-offs must be essential to running a business and common in the business’s industry.

What is the purpose of an accounting write-off?

In any case, accounting write-offs serve two purposes: Firstly, write-offs support accounting accuracy objectives Secondly, the “write-off” creates tax savings for asset owners. These actions reduce tax liability by creating (non-cash) expenses that result in lower reported income.

Are there any write offs for a Solopreneur?

Being self-employed means that we get some juicy write-offs for our business. Learn 7 awesome write-offs that all solopreneurs should be taking. Home About Podcast Blog Courses Money Masterclasses Bad Ass Business Finance Quick & Dirty QuickBooks Mini-Trainings Work With Me QuickBooks Online Help Income Forecasting What People Are Saying Contact

What’s the difference between a write down and a write-off?

Write-off is an accounting term referring to an action whereby the book value of an asset is declared to be 0. A write-down also lowers asset book value, but it does not take the value to 0. In either case, the loss enters the accounting system as an expense.