How do I lower my personal tax liability?

The key to minimizing your tax liability is reducing the amount of your gross income that is subject to taxes. Putting pre-tax dollars into a retirement plan like a 401(k) is one easy way to reduce your taxable income for the year.

How do you calculate minimum tax liability?

How Does the AMT Calculation Work?

- Calculate taxable income.

- Add back preferential tax items, such as capital gains, to establish an individual’s minimum tax amount.

- Add back 30% of capital gains (which means 80% of capital gains will now be taxable, instead of the normal 50%) for minimum tax calculations.

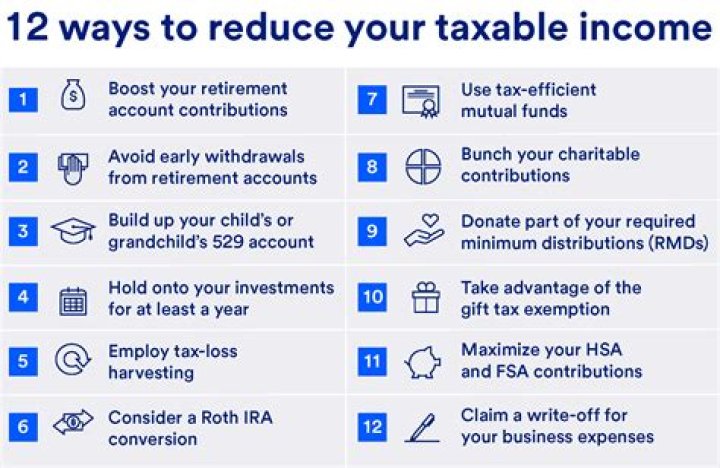

15 Legal Secrets to Reducing Your Taxes

- Contribute to a Retirement Account.

- Open a Health Savings Account.

- Use Your Side Hustle to Claim Business Deductions.

- Claim a Home Office Deduction.

- Write Off Business Travel Expenses, Even While on Vacation.

- Deduct Half of Your Self-Employment Taxes.

- Get a Credit for Higher Education.

Does becoming a homeowner lower your income tax liability?

The main tax benefit of owning a house is that the imputed rental income homeowners receive is not taxed. Although that income is not taxed, homeowners still may deduct mortgage interest and property tax payments, as well as certain other expenses from their federal taxable income if they itemize their deductions.

How can your parents help reduce your tax liability?

Your parents can help bring down your tax liability in several ways. Here are some smart strategies that can reduce your tax outgo. In this article we have listed four tips to save Tax Through Your Parents which includes 1.

How can I reduce my income tax liability?

If you sell an investment that has lost value, you can use that loss to offset other income. The income tax you pay each year is based on your gross income, and for many of us, the easiest way to reduce that figure is by contributing to an employer-sponsored retirement plan or individually held traditional IRA.

How can I avoid tax if my parents have a high income?

If any or both of your parents do not have a high income but you have an investible surplus, you can avoid tax by transferring money to them which can then be invested in their name.

How does owning an asset affect your tax liability?

If you owned the asset for less than a year, it’s a short-term gain so it’s added to your tax liability as ordinary income and it’s taxed according to your tax bracket. These factors are just the beginning of your tax liability. The Internal Revenue Code (IRC) kindly allows you to whittle away at your taxable income with various deductions.