How do you analyze cash flow from rental property?

The 50% Rule states that a rental property’s net cash flow should be at least 50% of the gross rent less the mortgage payment (P&I): Net cash flow = (Gross rent x 50%) – Mortgage P&I. ($12,000 gross annual rent x 50%) – $4,296 mortgage P&I = $1,704 per year.

Can you pay yourself for managing rental property?

You can pay yourself a fee for managing your own rental property, but this may not be the wisest course of action. When you transfer money from your business banking account to your personal account, the IRS will see this as income, and you will be taxed accordingly.

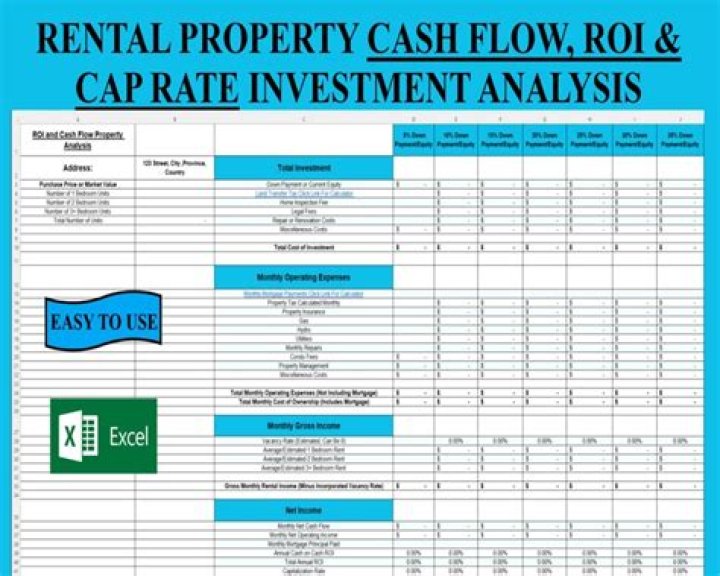

Calculating a rental property’s cash flow is a relatively simple process:

- Determine the gross income from the property.

- Deduct all expenses relating to the property.

- Subtract any debt service relating to the property.

- The difference is the property’s cash flow.

Can a disregarded SMLLC member own real estate?

Here’s where it gets even more interesting. The disregarded SMLLC’s member (this could be you) is considered to directly own for federal income tax purposes any real estate that is actually owned by the disregarded SMLLC.

Can a SMLLC exchange real estate for a replacement property?

Therefore, an exchange of property owned by your SMLLC will be treated as an exchange by you personally for purposes of the Section 1031 like-kind exchange rules. Under these rules, you can potentially swap appreciated real estate for a replacement property (or properties) while owing little or nothing to Uncle Sam.

Can a rental property increase its cash flow?

You can raise rents if the rental market is strong, but this can be a delicate balance because it might increase vacancies. The loss of income from more vacant units can easily wipe out any gains from increased rents. This is by no means the only way to calculate cash flow for a rental property, although it might well be the easiest.

Can a SMLLC be treated as a separate corporation?

Specifically: * Disregarded SMLLCs are treated as separate corporations for federal employment tax purposes.