How do you calculate current year depreciation?

Straight-Line Method

- Subtract the asset’s salvage value from its cost to determine the amount that can be depreciated.

- Divide this amount by the number of years in the asset’s useful lifespan.

- Divide by 12 to tell you the monthly depreciation for the asset.

Why do we calculate depreciation every year?

The purpose of depreciation is to represent an accurate value of assets on the books. Every year, as assets are used, their values are reduced on the balance sheet and expensed on the income statement.

Is depreciation calculated in the year of sale?

First, to establish account balances that are appropriate at the date of sale, depreciation is recorded for the period of use during the current year. Second, the amount received from the sale is recorded while the book value of the asset (both its cost and accumulated depreciation) is removed.

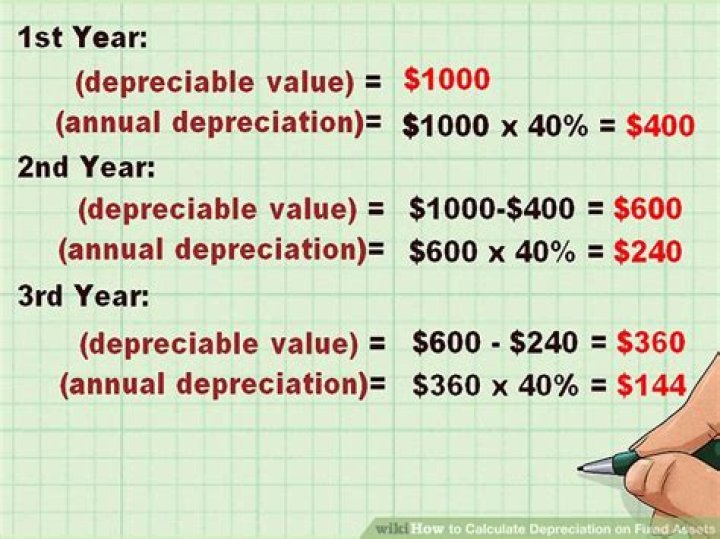

Is depreciation calculated in the first year?

Depreciation is calculated each year for tax purposes. The first-year depreciation calculation is: Cost of the asset – salvage value divided by years of useful life = adjusted cost. The next year’s calculation is based on the previous year’s total.

Why is depreciation calculated at the end of the year?

Accountants use depreciation to account for the wear and tear on business assets over time. As depreciation is a noncash expense, the amount must be estimated. Each year a certain amount of depreciation is written off and the book value of the asset is reduced.

How is depreciation calculated for the first year?

Depreciation is calculated each year for tax purposes. The first-year depreciation calculation is: Cost of the asset – salvage value divided by years of useful life = adjusted cost. Each year, use the prior year’s adjusted cost for that year’s calculation. The next year’s calculation is based on the previous year’s total.

What is the depreciation rate for 40 units?

For 40 units, the depreciation table will be as follows: # Depreciation expense for the Year 2028 is kept at $96,871 to maintain the residual value at the end of 10 Years. It helps to spread the cost of an investment in fixed assets across the useful life of the asset.

When does partial year depreciation take place on an asset?

Depending on different accounting rules, depreciation on assets that begins in the middle of a fiscal year can be treated differently. One method is called partial year depreciation, where depreciation is calculated precisely when assets start service and the convention (schedule) in which the depreciation occurs.

Which is the most commonly used method of depreciation?

The most widely used method of depreciation is the straight-line method. This rate is calculated as per the following formula: Depreciation Value per year = (Cost of Asset – Salvage value of Asset)/ Depreciation Rate per Year Cost of asset: It is the initial book value of the asset.