How long after I refinance can I buy another house?

How soon after refinancing can I buy another home? If you plan to buy a vacation home or an investment property, you can buy as soon as your refinance closes and you have the cash in hand. However, you cannot buy a separate primary residence using a cash-out refinance and then move into it right away.

Is it possible to refinance home for what it’s worth and get cash out?

When you refinance, you can do anything you want with the money you take from your equity. You can make repairs on your property, catch up on your student loan payments or cover an unexpected medical or auto bill. Cash-out refinances also usually give you access to lower interest rates than credit cards.

What happens to the money from a cash out refinance?

Then when your new loan exceeds what you owe on your existing mortgage, you get the difference in cash. Cash-out refinances under Fannie Mae guidelines let borrowers use the proceeds to pay debts such as the first mortgage or take out equity to be used for other purposes, among other things.

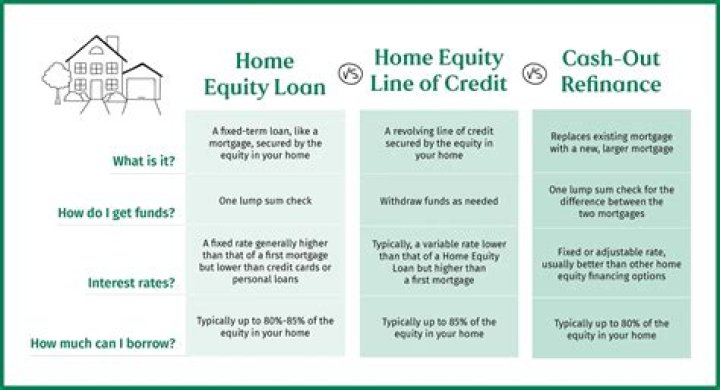

What’s the difference between home equity line of credit and cash out refinance?

Cash-out refinancing, home equity loans and home equity lines of credit (HELOC) are all methods of capitalizing on your home’s value, but there are important differences. A cash-out refinance replaces your existing mortgage with a higher loan amount, while home equity loans and lines of credit are additional mortgages.

When to refinance your home with Fannie Mae?

Cash-out refinances under Fannie Mae guidelines let borrowers use the proceeds to pay debts such as the first mortgage or take out equity to be used for other purposes, among other things. But to qualify for a cash-out refinance, you must wait at least six months since the purchase of the property.

What happens when you take out a cash out mortgage?

Unlike when you take out a second mortgage, a cash-out refinance doesn’t add another monthly payment to your list of bills – you pay off your old mortgage and replace it with your new mortgage. For example, let’s say that you bought a home for $200,000 and you’ve paid off $60,000. This means you still owe $140,000 on your home.