How long are closing costs depreciated?

27.5 years

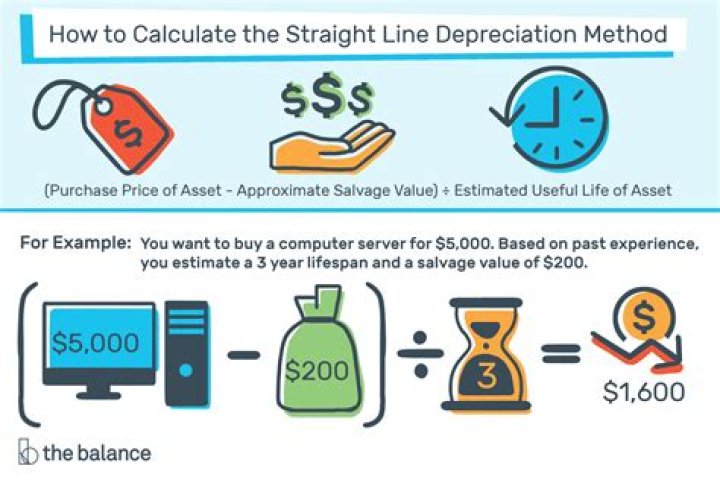

For real property, that schedule is over a period of 27.5 years (under a method called Modified Accelerated Cost Recovery System or MACRS). That means that you take the total basis of the property, divide it by 27.5, and that is the amount that you can depreciate each year.

When did the tuition and fees deduction expire?

The Tuition and Fees Deduction expired at the end of 2016 but was renewed for the 2017 tax year with the Bipartisan Budget Act of 2018. The Further Consolidated Appropriations Act, 2020 extended the expiration date for the Tuition and Fees Deduction to December 31, 2020.

Can you claim expenses for previous tax years?

You must claim within 4 years of the end of the tax year that you spent the money. If your claim is for previous tax years, HMRC will either make adjustments through your tax code or give you a tax refund.

Closings costs on a rental property fall into one of three categories: Deduct upfront in the current year. Amortize over the loan term. Add to basis (capitalize) and depreciate over 27.5 years.

Do closing costs get depreciated?

Basis, Closing Costs, and Capital Expenses As you depreciate the property, the costs used to close on the house will essentially be depreciated, as well. Therefore, you actually deduct the closing costs over time, rather than deducting most of them immediately when you purchase the real estate.

How much of the closing cost is tax deductible?

closing costs tax-deductible. There is no clear-cut answer on whether closing costs are tax-deductible, because no two closing cost situations are the same. Depending on factors such as personal wealth, tax bracket, home cost, permanent residence location and related fees, you can be anywhere from 10% to 90% exempt.

Can you deduct closing costs on a refinance loan?

Points paid on a home improvement refinance loan. In cases where you used only a portion of your loan proceeds for home improvement, any additional points can be deducted over the remaining loan term. Closing costs that can be deducted when you sell your home.

Where do I put my closing costs on my tax return?

The amount you can deduct should be included in box 5 of your mortgage tax form 1098. Tax-deductible costs may include: Upfront mortgage insurance premiums ( UFMIP ) and mortgage insurance premiums (MIP) paid on a loan insured by the Federal Housing Administration (FHA).

What are the closing costs for a new home?

These may include: Owner’s title insurance. An owner’s title insurance policy protects you against prior ownership claims on the property. Property taxes. Only applicable if you paid any share of the seller’s taxes when you bought your home. Title fees when you buy. These costs may include escrow, endorsements and other title search fees.