How long do you amortize goodwill for tax purposes?

15 years

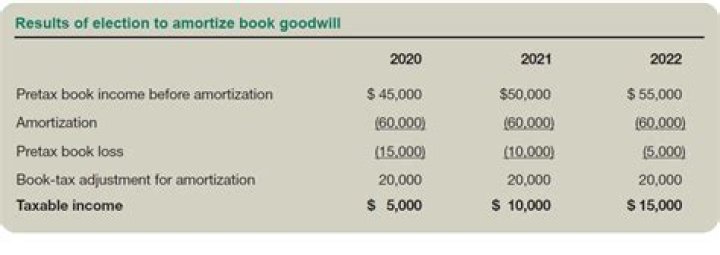

Any goodwill created in an acquisition structured as an asset sale/338 is tax deductible and amortizable over 15 years along with other intangible assets that fall under IRC section 197. Any goodwill created in an acquisition structured as a stock sale is non tax deductible and non amortizable.

Is goodwill amortized over 10 or 15 years?

Goodwill can be amortized over 10 years or less, in which case the impairment test is simplified in addition to being trigger-based. In 2016 the FASB launched a project to simplify goodwill impairment testing for all companies, while maintaining its usefulness.

Can I amortize goodwill?

In accounting, goodwill is accrued when an entity pays more for an asset than its fair value, based on the company’s brand, client base, or other factors. Now, private companies can elect to amortize goodwill on a straight-line basis over 10 years, although this election is not required.

Why is amortization added back to cash flow?

Amortization expense refers to the depletion of intangible assets and can be a major source of expenditure on the balance sheet of some companies. Amortization is always a non-cash expense. Therefore, like all non-cash expenses, it must be added back to net earnings while preparing the indirect statement of cash flow.

Does goodwill have a useful life?

Goodwill cannot exist independently of the business, nor can it be sold, purchased, or transferred separately. As a result, goodwill has a useful life that is indefinite, unlike most of the other intangible assets.

How is goodwill impairment treated for tax purposes?

Impairment of Goodwill Tax Treatment The impairment of goodwill will also impact the financial statements differently than the tax return. Under GAAP, goodwill is tested for impairment at the reporting unit level. For tax purposes, goodwill is not written off until the reporting unit is sold or otherwise closed.

What happens when goodwill is impaired?

If a company doesn’t test for goodwill impairment, it could overstate its value or net worth. Since goodwill is an intangible asset, treating it like a normal asset and amortizing it does not give a clear picture as to the value of the asset. It needs to be tested for impairment once a year.

Can you depreciate goodwill under IFRS?

Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life. If the fair market value goes below historical cost (what goodwill was purchased for), an impairment must be recorded to bring it down to its fair market value.

Is goodwill Amortised or impaired?

Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life. Instead, management is responsible for valuing goodwill every year and to determine if an impairment is required.

Any goodwill created in an acquisition structured as an asset sale/338 is tax deductible and amortizable over 15 years along with other intangible assets that fall under IRC section 197.

Is goodwill always amortized?

What do you need to know about goodwill amortization?

It’s a value based on expected continued customer patronage, due to its name, reputation, or any other cause. Tax reporting for Goodwill amortization means you’re deducting the Goodwill over time on your business tax returns e.g. Form 1120 for C Corporations, Form 1120-S for S Corporations, Form 1065 for Partnerships, Schedule C, Schedule E etc.

When to use the new standard for goodwill impairment?

The new standard mandates the impairment of goodwill even in instances where the decrease in the reporting unit’s fair value might have been caused by a reduction in the fair value of financial assets carried at amortized cost rather than a decline in the fair value of goodwill.

Can a company test goodwill and long lived assets at the same time?

Exhibit 1 reflects goodwill impairment alternatives under different scenarios. If companies test goodwill and long-lived assets (held and used) at the same time because of a triggering event, they must follow a certain order in their impairment testing.

When do you record goodwill impairment on a balance sheet?

Goodwill impairment is an accounting charge that companies record when goodwill’s carrying value on financial statements exceeds its fair value. Pooling-of-interests is a former method of accounting governing how the balance sheets of two companies were combined in an acquisition or merger.