How long does it take for you to get your check after you refinanced and closed?

No. You won’t receive the funds until three to five days after closing. The Truth in Lending Act requires your lender to give you three business days after closing to cancel the refinance. Since the loan isn’t technically closed until after that time passes, you won’t receive your funds until then.

When you refinance can you claim on taxes?

You can deduct the full amount of interest you pay on your loan in the last year if you did a standard refinance on a primary or secondary residence. You can only deduct 100% of your interest if you take a cash-out refinance, particularly if you use the money for a capital home improvement.

Does refinancing change your basis?

Most closing costs for the refinance of an investment property are not deductible. The mortgage interest and property taxes can be deducted, but the rest are added to the cost basis for the asset and are depreciated.

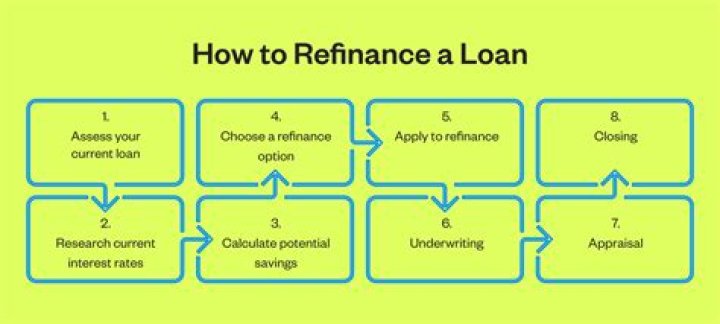

How long is closing after underwriting?

The full mortgage loan process often takes between 30 and 45 days from underwriting to closing.

How much can you claim on taxes when you refinance a home?

Let’s also say that your refinanced loan has 10 years left on its term. You would only be able to deduct $500 per year from your federal taxes. However, you can claim this deduction every year until your loan matures. The same rules apply for closing costs on a rental property refinance.

How often can you claim closing costs on a refinance?

However, you can claim this deduction every year until your loan matures. The same rules apply for closing costs on a rental property refinance. For example, if you spent $15,000 on closing costs for a 15-year refinance, you’d deduct $1,000 a year until your loan matures.

Is the mortgage insurance deduction still available for refinance?

It also removed the insurance deduction on most mortgage loans. However, subsequent Congressional action restored the mortgage insurance deduction through the 2020 tax year. In the next section, we’ll go over a few specific deductions you can take advantage of during the year you refinance and beyond.

What happens if I refinance my mortgage in February 2019?

So, if you took a $900,000 mortgage in February 2016 and refinanced it in February 2019 in a straight rate-and-term refinance transaction, interest paid on the entire remaining balance of nearly $852,000 would still be eligible for the mortgage interest deduction, as the old limits for acquisition debt are carried forward.