How long does offer subject to finance last?

A 14-21 day finance clause is most common but a longer timeframe can be negotiated with the vendor.

How long does a buyer have to secure financing?

The buyer and seller must agree on the timeframe in which the buyer needs to secure mortgage approval. A contingency period typically lasts anywhere between 30 and 60 days. If the buyer isn’t able to get a mortgage within the agreed time, then the seller can choose to cancel the contract and find another buyer.

Why does financing fall through when buying a house?

One of the most common reasons a pending sale falls through is that the buyer isn’t able to qualify for financing. To receive a pre-approval letter, the lender has typically checked the buyer’s credit, verified their documentation, and approved them for a specific loan amount, according to Investopedia.

Why does financing fell through on a house?

Do most loans have a due-on-sale clause?

Do all mortgages have a due-on-sale clause?: Although the majority of mortgages contain due-on-sale clauses, there are still some mortgages that are assumable. Such mortgages include VA, FHA and USDA loans. Even though these types of loans are assumable, prospective buyers must still qualify for the loan.

Who holds the deposit on a house purchase?

As the successful bidder on the property, your deposit should be held in trust by the real estate brokerage of the seller’s agent. In the rare and extreme case that you have a dispute with the seller, they can hold onto your deposit or keep it as damages, but they can’t just take the money and run.

What happens if you buy a house and financing falls through?

The homebuyer’s lender appraises the property at a value significantly lower than the agreed-upon purchase price. If the buyer can’t make up the shortfall from savings or the seller won’t lower the price, the buyer can no longer afford the property. There are title insurance or home inspection surprises.

Can your loan fall through after closing?

Mortgage approvals can fall through on closing day for any number of reasons, like getting the proper financing, appraisal or inspection issues, or contract contingencies.

What does it mean to take property subject to a mortgage?

The term “taking subject to” is when the buyer incurs no liability to repay the loan. The loan stays in the seller’s name, but the buyer gets the deed and therefore controls the property. Although the buyer makes the mortgage payments, the seller remains responsible for the loan.

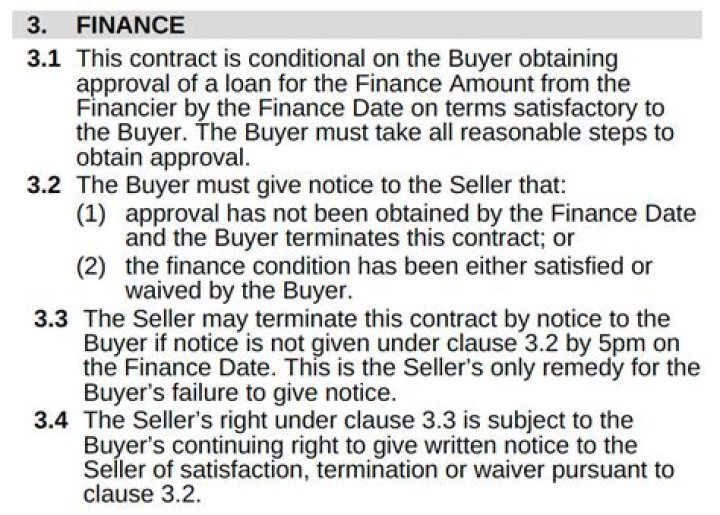

How does an offer subject to finance work?

Making your price offer ‘Subject to Finance’ is a clause that can be included in the sales contract. It means that your offer is conditional on the lender approving the finance you need to buy the property. If your loan application is refused you can terminate the contract and recoup your deposit.

What does it mean to buy a house subject to an existing mortgage?

Buying “subject to” means buying a home subject to the existing mortgage. It means the seller is not paying off the existing mortgage, and the buyer is instead taking over the payments.

What does it mean when a house is subject to finance?

If a home sale is “subject to finance” it means that the transaction will pend until the buyer’s home loan (or ‘finance’) has been approved by their lender. If the loan isn’t approved, then the prospective buyer can opt out of the sale, generally without any legal or financial liability. Do I need ‘subject to finance’ in my house offer? Yes.

Can you buy a property subject to an existing loan?

Taking over a property “Subject To” an existing loan is not as hard as it may seem as long as you know what it is. If you know what it is and how to explain it to the seller, and what steps to use to protect the loan from being called, you can buy many more properties faster than you can if you have to go get new loans on each purchase.

What happens if I buy a property subject to?

However, if you don’t make the payments and you lose the property, there will be no personal liability beyond the loss of the property. Typically homeowners who are behind on payments, in foreclosure or have no equity in the home are the most common types of motivated sellers you will be dealing with and perfect for buying “subject to”.