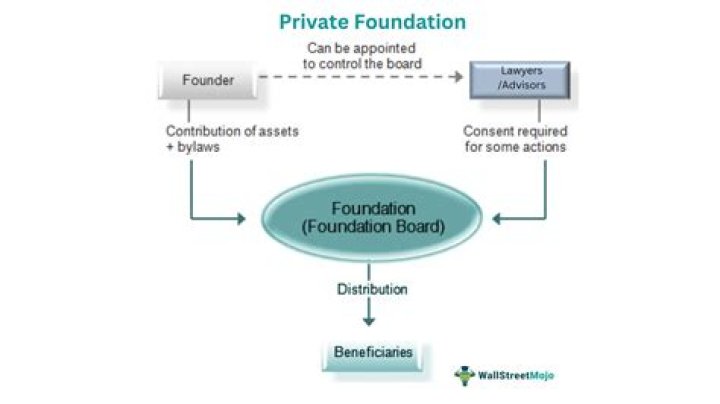

How much does a private foundation have to distribute?

Generally, a private foundation must meet or exceed an annual payout requirement of five percent of the average market value of its net investment assets to avoid paying taxes.

What is a qualifying distribution for a private foundation?

In general, a qualifying distribution includes any amount paid by the foundation to accomplish its 501(c)(3) purposes, such as the following: Grants. This type of payment is the quintessential qualifying distribution, and how many foundations meet the bulk of their requirement.

How long does a private foundation have to distribute?

Private foundations have 12 months after the tax year in question to satisfy the minimum payout requirement. For example, a new foundation could pay out nothing in its initial tax year and satisfy the first year’s minimum by applying the first expenditures in the second year retroactively.

Can a private foundation make a grant to another private foundation?

Can a private foundation make a grant to an organization other than a public charity? Yes, it can. Technically, grants to entities other than public charities are “taxable expenditures” and are subject to a dreaded excise tax.

Can private foundations fundraise?

Yes—a private foundation can raise money from “outsiders”, including family friends, company vendors and employees. A private foundation is a section 501(c)(3) organization, and while private foundations have special rules, no rule prohibits the organization from receiving charitable contributions.

Qualifying distributions by private foundations, in general, are any amounts paid to accomplish religious, charitable, scientific, literary, or other public purposes. A portion of administrative expenses can be also allocated and treated as qualifying distributions.

Can a QCD go to a private foundation?

Qualified charitable distributions can be made only to certain qualified charitable organizations, as defined in the tax code. Currently, QCDs cannot be made to donor-advised fund sponsors, private foundations and supporting organizations, though these are categorized as charities.

Generally speaking, a private foundation that is not a private operating foundation is required to distribute annually – through grants and grant-related expenses – at least 5% of the total fair market value of its noncharitable-use assets from the preceding year.

How are private foundations affected by the 5% rule?

Utilizing a more formal spending policy may allow the private foundation to manage distributions from year to year while still planning ahead to meet the 5% distribution requirement. Private foundations should carefully manage the grant commitments that they make to recipient organizations.

How are not for profit organizations dependent on private foundations?

Furthermore, many other not-for-profit organizations are dependent on the grants they receive from private foundations. If the amount that private foundations will award to such organizations is linked to investment returns in a given year, then these grant recipients and those they serve are also at the mercy of equity market return fluctuations.

What is the 5% minimum distribution rule?

The 5% Minimum Distribution Rule In general, Section 4942 of the Internal Revenue Code requires private foundations to distribute 5% of the fair market value of their assets each year.