How much income do you need to contribute to a Roth IRA?

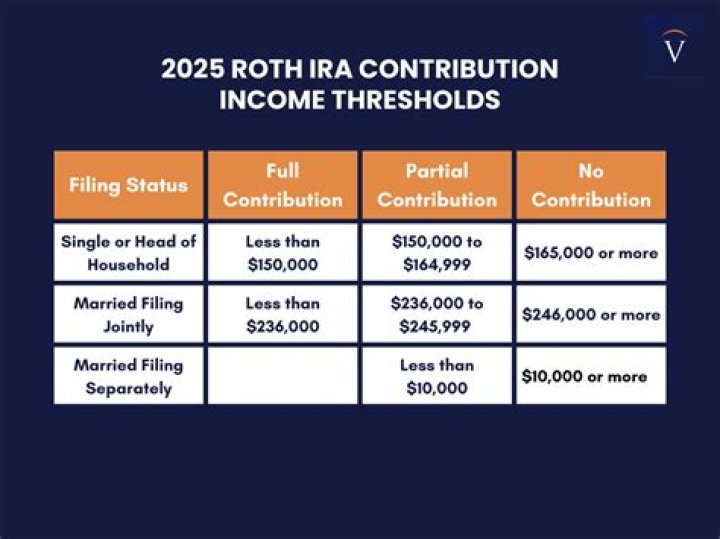

You must be under the income limit. To contribute to a Roth IRA, your 2021 modified adjusted gross income must be $140,000 (single filers) or $208,000 (married filing jointly). (IRS Publication 590-A, Worksheet 2-1 has complete instructions on figuring MAGI for Roth IRAs.) You have to have earned income.

How much can I contribute to a Roth IRA in 2020?

$6,000

The maximum amount you can contribute to a Roth IRA for 2020 is $6,000 if you’re younger than age 50. If you’re age 50 and older, you can add an extra $1,000 per year in “catch-up” contributions, bringing the total contribution to $7,000. (The limits were the same for 2019.)

Should I contribute to Roth IRA monthly or yearly?

Sometimes, cash flow can be a temporary problem, but even if you can’t put in money every single month, you should make every effort to contribute at least once a year to your IRA account. For many people, an annual contribution is the most practical solution because of the way their income/expense cycle works.

If you file taxes as a single person, your Modified Adjusted Gross Income (MAGI) must be under $139,000 for the tax year 2020 and under $140,000 for the tax year 2021 to contribute to a Roth IRA, and if you’re married and file jointly, your MAGI must be under $206,000 for the tax year 2020 and 208,000 for the tax year …

Can I make a one time contribution to my Roth IRA?

You can contribute only as much as you earn in any given year (up to the standard contribution limit), but you don’t have to wait until you earn the money, Kahler says. “Say all your money comes in in December. You can make the contribution in January as long as you have funds to make it.

Are ROTH IRAs tax deductible?

While not tax-deductible, contributions to a Roth IRA give you the opportunity to create a tax-free savings account. You can use this account in retirement or leave it as an inheritance for your heirs. Roth IRAs offer many of the advantages of regular IRAs, but with more flexibility.

Will opening a Roth IRA lower my taxes?

Yes, you can lower your taxable income and your tax bill by contributing to an individual retirement account (IRA).

When do I have to contribute to a Roth IRA?

Roth IRAs offer tax-free growth on both the contributions and the earnings that accrue over the years. If you play by the rules, you won’t pay taxes when you take the money out. 1 In 2020 and 2021, the contribution limits are set at $6,000, and an additional $1,000 may be contributed by those who are age 50 or older. 2

What’s the maximum annual contribution to a Roth IRA?

The maximum total annual contribution for all your IRAs combined is: $6,000 if you’re under age 50 $7,000 if you’re age 50 or older Roth IRA Contribution Limits (Tax year 2021)

Is there a tax deductible contribution to a Roth IRA?

Traditional IRA contributions are deductible, but the amount you can deduct may be reduced or eliminated if you or your spouse is covered by a retirement plan at work. Lower-income taxpayers may be eligible for the “saver’s credit” if they contribute to an IRA. For 2020, the most you can contribute to your Roth and traditional IRAs is a total of:

Are there income limits on converting a traditional IRA to a Roth IRA?

When you convert a traditional IRA to a Roth IRA that is not considered a contribution – so Roth conversion amounts are not subject to the limits above. It used to be that if your income was over $100,000, you could not convert IRA money to a Roth, but that tax law changed, and that income limit was removed in 2010.