Is a second-hand van tax deductible?

Regardless of the method used to purchase the vehicle, the initial cost or finance costs are not tax deductible when you acquire a vehicle personally. Additionally you will not be able to claim tax relief on running costs such as road tax, insurance, fuel and servicing.

What are my rights when buying a second-hand van?

The Act states the car must be “of a satisfactory quality”, “fit for purpose” and “as described”. (For a used car, “satisfactory quality” takes into account the car’s age and mileage.) You have a right to reject something faulty and you’re entitled to a full refund within 30 days of purchase in most cases.

Can I get my money back from a private car sale?

After a vehicle is sold from one private party to another, the buyer can ask for their money back, but the seller generally does not have to agree to cancel the sale, absent a warranty or fraud.

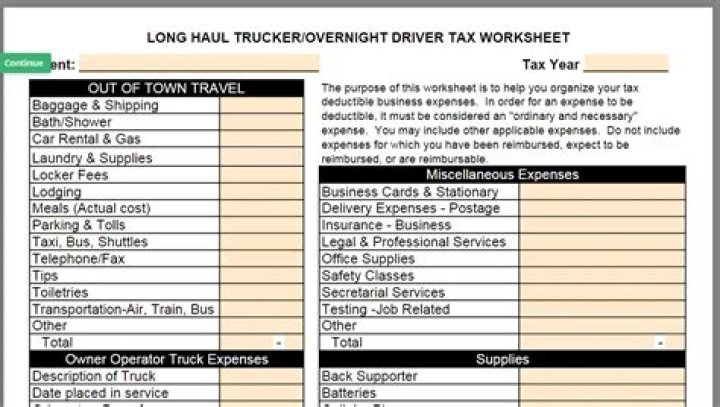

Can a business claim the cost of a van?

Best Answer. Vans come under the scope of Capital Allowances for businesses. You can therefore claim the cost of the van against your expenses, as part of the Annual Investment Allowance (AIA) that a business is able to offset against tax.

Can a second hand van be sold without VAT?

A second hand van can be sold as a margin scheme vehicle, where is was purchased without VAT charged by the previous (private) owner. Vans, like cars, can be included in the scheme. And the scheme can be used for one-off transactions, without the need to full record-keeping requirements.

Can a company buy a van and claim back VAT?

Dear ***** I have a client who wants to buy a van and claim back the VAT. He is not registered for VAT. Could he register claim back the VAT and … read more A COMPANY OWNER DECIDES TO BUY A VAN FOR HIS BUSINESS. IF A COMPANY OWNER DECIDES TO BUY A VAN FOR HIS BUSINESS. IF HE DECLARES THE VAN ON A P11D RETURN FOR BOTH … read more

Can a dealer use a second hand scheme?

This means that they only account for VAT on the profit margin, but your business will be unable to recover this VAT as it is a condition of the use of the second-hand scheme. The use of a second-hand scheme by a dealer is not compulsory and they sell goods either using the scheme or not.