Is an IRA considered retirement income?

An individual retirement account (IRA) allows you to save money for retirement in a tax-advantaged way. Traditional IRA – You make contributions with money you may be able to deduct on your tax return, and any earnings can potentially grow tax-deferred until you withdraw them in retirement.

Which IRA is not taxed when you retire and take the money?

Roth IRA

While you don’t get a tax deduction in the year you contribute to a Roth IRA or Roth 401(k), you don’t have to pay income tax on the investment growth in the account and withdrawals in retirement from an account at least five years old are typically tax-free.

Traditional IRAs and 401(k)s Savers love these tax-deferred retirement accounts. Contributions to the plans generally reduce their taxable income, saving them money on their tax bills in the current year. Their savings, dividends and investment gains within the accounts continue to grow on a tax-deferred basis.

Can you contribute to an Individual Retirement Account ( IRA )?

Choices include banks, brokerage companies, federally insured credit unions, and savings and loan associations. Most individual investors open IRAs with brokers. Note that you can only contribute to an IRA with earned income that meets IRA rules. Income from investments, Social Security benefits, or child support does not count as earned income.

Can you deduct the cost of an IRA at work?

Traditional IRAs. Retirement plan at work: Your deduction may be limited if you (or your spouse, if you are married) are covered by a retirement plan at work and your income exceeds certain levels. No retirement plan at work: Your deduction is allowed in full if you (and your spouse, if you are married) aren’t covered by a retirement plan at work.

What happens to your taxes when you put money into an IRA?

If someone puts $6,000 into an IRA, that person’s taxable income decreases by the amount of the contribution. However, when that individual withdraws money from the account during retirement, those withdrawals are taxed at their ordinary income tax rate.

Can a 50 year old make a catch up contribution to an IRA?

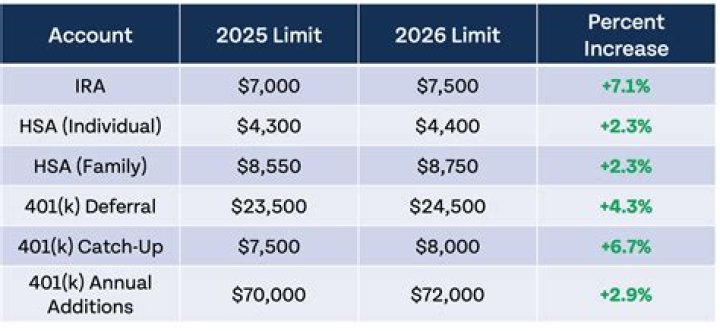

An IRA plan is an investment account individuals may establish to save for retirement. A catch-up contribution is a type of retirement savings contribution that allows people age 50 or older to make additional contributions to their 401(k) accounts and/or individual retirement accounts (IRAs).