Is deferred compensation FICA taxable?

Under the special timing rule, deferred amounts are generally treated as wages for purposes of FICA taxes when the deferred compensation is no longer subject to a substantial risk of forfeiture (i.e., upon vesting). The social security portion of FICA tax is only imposed on wages up to the social security wage base.

Are deferred compensation payments subject to FICA?

Special Timing Rule for FICA Tax on Deferred Compensation Wages are generally subject to FICA tax when they are paid, whether actually or constructively, to the employee. Therefore, immediately vested amounts (e.g., salary deferrals) are subject to FICA tax at the time these amounts are withheld from pay.

Are Nqdc contributions tax deductible?

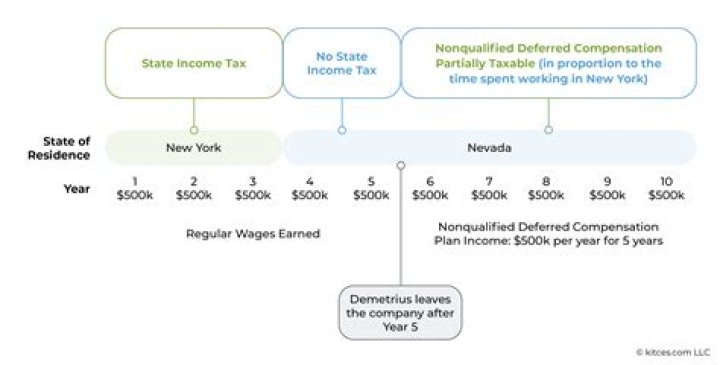

If a NQDC plan provides for contributions and “earnings” on the contributions, both the contributions and the earnings are eventually taxed as compensation. Under a NQDC plan, employers can only deduct the benefit as the employee includes the benefit in taxable income.

What should I do with my 457 B when I retire?

Once you retire or if you leave your job before retirement, you can withdraw part or all of the funds in your 457(b) plan. All money you take out of the account is taxable as ordinary income in the year it is removed. This increase in taxable income may result in some of your Social Security taxes becoming taxable.

How are deferred compensation taxes calculated for FICA?

For the purpose of calculating FICA wages, amounts taken into account as deferred compensation are combined with other amounts paid to the employee that constitute wages for that tax year, and FICA taxes are imposed on this combined amount.

How is the FICA tax calculated for self employed?

To calculate your FICA tax burden, you can multiply your gross pay by 7.65%. Self-employed workers get stuck paying the entire FICA tax on their own. For these individuals, there’s a 12.4% Social Security tax, plus a 2.9% Medicare tax.

How are FICA taxes withheld and remitted to employees?

Typically, the FICA taxes are withheld and remitted by the employer at the time the compensation is distributed to the employee (i.e., the “General Timing Rule”). However, there is a “Special Timing Rule” that applies when the compensation is part of a nonqualified deferred compensation (“NQDC”) plan.

What are the tax rates for Social Security and FICA?

The breakdown for the two taxes is 6.2% for Social Security (on wages up to $137,700) and 1.45% for Medicare (plus an additional 0.90% for wages in excess of $200,000). Also known as payroll taxes, FICA taxes are automatically deducted from your paycheck.