Is GAAP a tax-basis?

Key differences When comparing GAAP and tax-basis statements, one difference relates to terminology used on the income statement: Under GAAP, businesses report revenues, expenses and net income. Tax-basis entities report gross income, deductions and taxable income.

What is GAAP accounting basis?

Generally accepted accounting principles, or GAAP, are a set of rules that encompass the details, complexities, and legalities of business and corporate accounting. The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices.

Does IRS follow GAAP?

The Internal Revenue Services (IRS) is a government agency primarily responsible for collecting taxes and administering statutory tax laws. Generally Accepted Accounting Principles (GAAP) regularly follows a set of accounting rules and principles that govern the standards for year-end financial reporting.

Does GAAP allow cash accounting?

Cash basis accounting is an accounting system that recognizes revenues and expenses only when cash is exchanged. Cash basis accounting is not acceptable under the generally Acceptable Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS).

What is the difference between GAAP and adjusted?

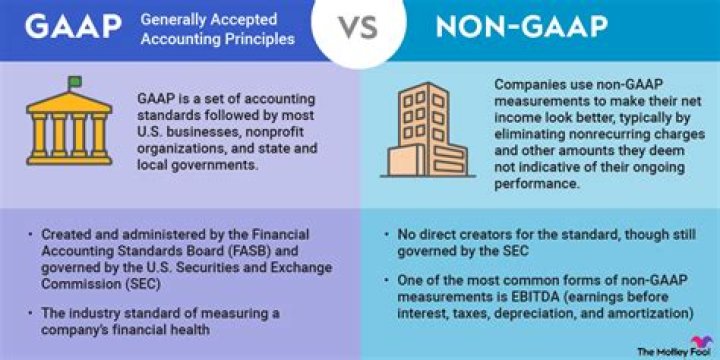

GAAP accounting standards offer uniformity in how companies report their financial performance. These actions usually come with large one-time costs that distort company profits. As such, a company will also provide an “adjusted” earnings number that excludes these nonrecurring items.

Why is GAAP necessary in accounting?

Why we need GAAP The purpose of GAAP is to ensure that financial statements of U.S businesses (and perhaps worldwide one day) are consistent and comparable. Without uniformity of accounting principles, investors are unable to interpret an international company’s accounting information.