Is it true that all amounts received from a life insurance annuity are taxable?

Annuities are tax deferred. What this means is taxes are not due until you receive income payments from your annuity. Withdrawals and lump sum distributions from an annuity are taxed as ordinary income. They do not receive the benefit of being taxed as capital gains.

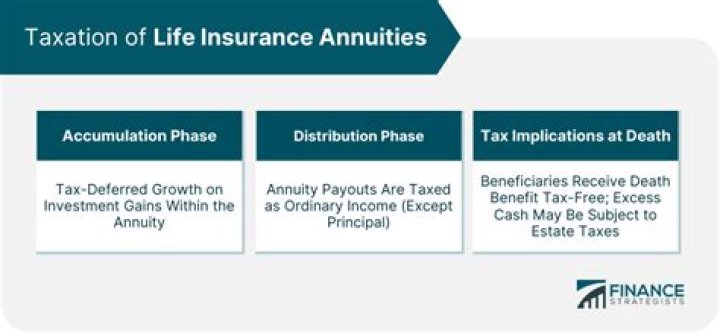

Annuities are tax deferred. But that doesn’t mean they’re a way to avoid taxes completely. Withdrawals and lump sum distributions from an annuity are taxed as ordinary income. They do not receive the benefit of being taxed as capital gains.

Are there any annuities that can not be inherited?

Some annuities can’t be inherited. If you purchase a single life or life only annuity, for example, the annuity would only pay benefits to you during your lifetime. There would be no death benefit to pass on to a beneficiary.

How does a life insurance annuity work when you die?

A life insurance annuity works like an income in that the death benefit is divided up over a number of years into equivalent amounts that the beneficiary receives each year. If you have life insurance and you’ve been keeping up with your premiums, when you die the life insurance company will pay out a death benefit to your beneficiaries.

Who is the beneficiary of an inherited annuity if one spouse dies?

There is a difference between a co-owner and a beneficiary. If a married couple owns an annuity jointly and one partner dies, the surviving spouse would continue to receive payments according to the terms of the contract. In other words, the annuity continues to pay out as long as one spouse remains alive.

When do you pay taxes on an inherited annuity?

The period of time when an annuity is being funded and before payouts begin is referred to as the accumulation phase . When a person inherits an annuity, the gains stay with the policy. Depending on the type of annuity, the tax will have to be paid on the lump sum received or on the regular fixed payments.