Is it worth not putting 20 down on House?

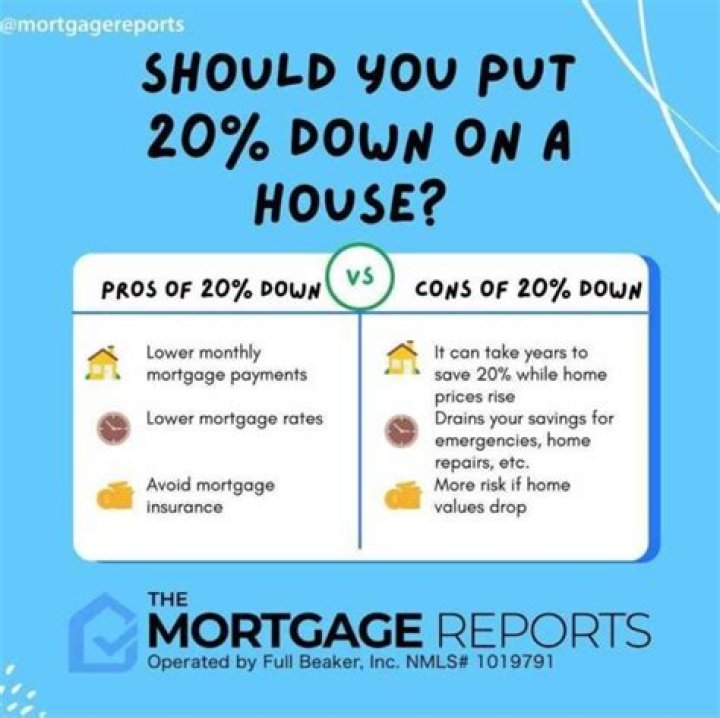

Putting at least 20% down can improve your chances of getting approved and locking in a lower rate (and monthly payment). Some lenders and programs will accept less than 20% down, but in most instances you’ll need to buy mortgage insurance.

How do I get around paying 20% down?

The first way is to look for a lender offering lender-paid mortgage insurance (LPMI), which eliminates PMI in exchange for a higher interest rate. Second, buyers can opt for a piggyback mortgage — one that uses a second loan to cover part of the down payment and reach 20%, therefore bypassing the PMI requirement.

Does 20 down guarantee a mortgage?

Consequently, more people are buying homes by putting less money down. Putting a full 20% down on mortgage ensures you won’t pay private mortgage insurance and will most likely get the lowest available interest rate.

Is it easier to get mortgage with 20 down?

Typically, mortgage lenders want you to put 20 percent down on a home purchase because it lowers their lending risk. It’s also a “rule” that most programs charge mortgage insurance if you put less than 20 percent down (though some loans avoid this). But it’s NOT a rule that you must put 20 percent down.

Why do you need a 20 percent down payment to buy a house?

A 20 percent down payment immediately puts equity into a property when you purchase it. That down payment safeguards you if the market turns downward temporarily. Trulia gives home buyers, sellers, owners and renters the inside scoop on properties, places and real estate professionals. Trulia has unique info on the areas people…

How much should you put down on a house?

Luckily, there are other options available to buyers, and you might be surprised to find that you can become a homeowner with a down payment of just 3% to 5%. In fact, there are valid reasons why it might be better to go for a lower down payment as opposed to making that 20% commitment.

How to buy a home in your 20s without going broke?

7 Tips For Buying A Home In Your 20s Without Going Broke 1. Know where you want to live. 2. Shore up your credit. 3. Get pre-approved for a mortgage. 4. Aggressively save for six to 12 months. 5. Research and leverage down payment assistance. 6. Do all your homework. 7. Don’t buy a home that you know you can’t afford.

How can I remain a 20 something homeowner?

This is probably the biggest key to remaining a 20-something homeowner. When you have a low salary, large student loan payments and other variables in your budget, it’s important to buy a home you can comfortably afford. Think of your mortgage, taxes, fees, insurance and maintenance in your budget as well.