Is loaning money taxable?

Because a loan means you’re borrowing money from a lender or bank, they aren’t considered income. Not only are all loans not considered income, but they are typically not taxable. The only time a loan would be considered income is if the loan was canceled by the lender or bank.

Are loan interests made to others taxable?

Typically, most interest is taxed at the same federal tax rate as your earned income, including: Interest on loans you make to others. Interest on certificates of deposit (CDs). Interest on U.S. obligations (except municipal bonds; U.S. Treasury bonds are federally taxable but not at the state level).

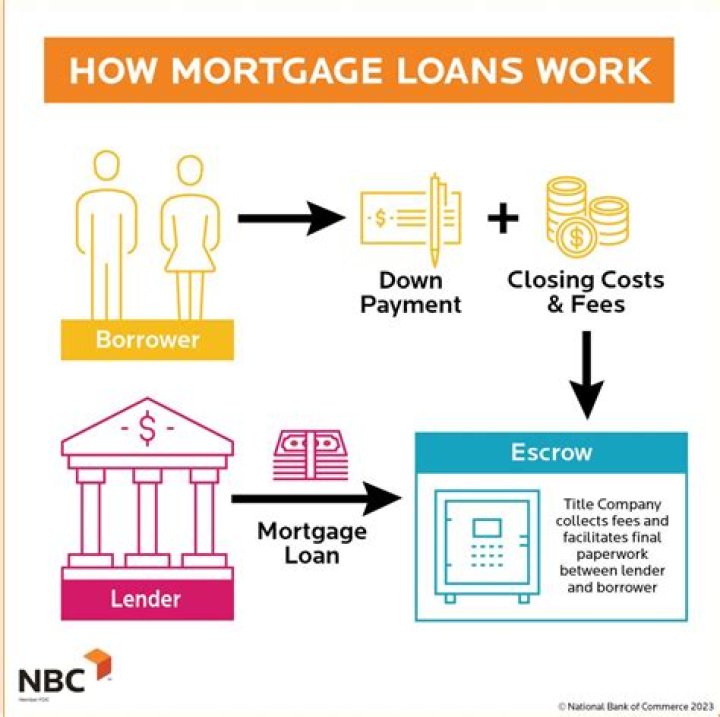

Can you get a loan without showing tax returns?

Can you get a mortgage without tax returns? Yes. There are many instances and different loan products that do NOT call for tax returns. This can be done whether or not your are self-employed.

How much tax do you pay on a$ 185, 000 salary?

You will pay $36,011.00 in Federal Tax on a $185,000.00 salary in 2021. How did we calculate Federal Tax paid on $185,000.00? How much Rhode Island State Tax should I pay on $185,000.00?

What’s the federal tax rate for$ 185K?

The $185k after tax calculation includes certain defaults to provide a standard tax calculation, for example the State of Rhode Island is used for calculating state taxes due.

What are the tax consequences of a family loan?

Tax consequences: When dealing with a family loan, the borrower and lender have to follow tax rules. Lenders may have to pay interest on income earned from the loan, as well as income not earned if they offer a below-market rate. Unless an exception applies, borrowers may have to repay the debt as agreed or claim the canceled debt as income.

When do I need to use the tax calculator?

This calculator helps you to calculate the tax you owe on your taxable income for the full income year. It can be used for the 2013–14 to 2019–20 income years.