Is pension paid by employer?

You and your employer must pay a percentage of your earnings into your workplace pension scheme. How much you pay and what counts as earnings depend on the pension scheme your employer has chosen. Ask your employer about your pension scheme rules.

Which employers still offer pensions?

14 Companies That Still Offer Pensions

- Coca-Cola. In addition to giving employees access to a 401k plan with a 3 percent company match, Coca-Cola also offers a defined benefit plan that is fully funded by the company.

- BB.

- NextEra Energy.

- Southern Company.

- General Mills.

- Lockheed Martin.

What is a pension from employer?

A pension is a retirement fund for an employee paid into by the employer, employee, or both, with the employer usually covering the largest percentage of contributions. When the employee retires, she’s paid in an annuity calculated by the terms of the pension.

Can my employer contribute to my personal pension scheme?

Your employer must automatically enrol you into a pension scheme and make contributions to your pension if you’re eligible for automatic enrolment. If your employer does not have to enrol you by law, you can still join their pension scheme if you want to. Your employer cannot refuse.

What are the two basic types of employer pension plans?

There are two basic types of retirement plans typically offered by employers – defined benefit plans and defined contribution plans.

What is the maximum I can pay into my workplace pension?

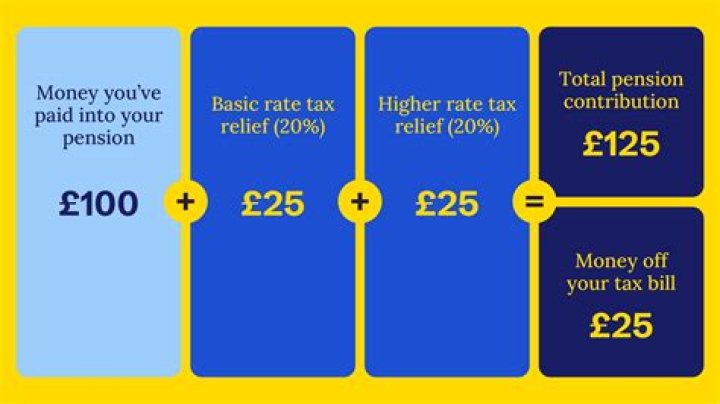

Maximum pension contributions The maximum is 100% of your relevant UK earnings (up to the annual allowance) or £3,600 gross, whichever is higher. If you go over this limit, this will result in a tax charge, known as the annual allowance charge.

What happens to my pension if I lose my job?

When you leave your employer, you do not lose the benefits you have built up in a pension and the pension fund belongs to you. If you’ve changed jobs and remember paying into a pension at your previous workplace, it’s likely you’ll have an old pension there.

What happens to my workplace pension when I die?

If the deceased hadn’t yet retired: Most schemes will pay out a lump sum that is typically two or four times their salary. If the person who died was under age 75, this lump sum is tax-free. This type of pension usually also pays a taxable ‘survivor’s pension’ to the deceased’s spouse, civil partner or dependent child.