Is refinancing a bad decision?

Refinancing your mortgage can be either a good or bad idea, depending on your motivation and goals as well as the financial terms of the refi. Homeowners who refinance can wind up paying more over time because of fees and closing costs, a longer loan term, or a higher interest rate that is tied to a “no-cost” mortgage.

Can you refinance with one person?

It is not possible to refinance with only one borrower on the application and still keep both your names on the mortgage. Other times, a couple or divorced couple might want to refinance to remove one person’s name from the mortgage. This is possible, but the borrower being removed needs to agree to the arrangement.

Should I refinance if I just did?

Some will argue that yes you should refinance again even though you just recently refinanced. According to Ben Edwards at Money Smart Life, if interest rates are 2% lower than your current rate, you should consider a refinance.

How long does it take to hear back about refinancing?

A refinance typically takes 30 – 45 days to complete. However, no one will be able to tell you exactly how long yours will take. Appraisals, inspections and other third parties can delay the process. Your refinance might be longer or shorter, depending on the size of your property and how complicated your finances are.

What are the steps of refinancing your home?

The Refinance Process – What to Expect

- Step One: Check Your Credit.

- Step Two: Compare Types of Loans.

- Step Three: Gather Documents.

- Step Four: Apply for a Loan.

- Step Five: Get an Appraisal.

- Step Six: Go Through Underwriting.

- Step Seven: Lock in Your Rate.

- Step Eight: Close Your Loan.

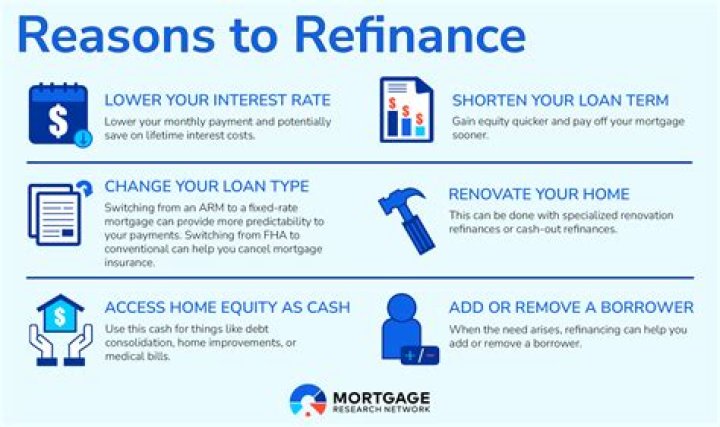

When is it a good idea to refinance your mortgage?

Mortgage refinancing is a good idea when you’ll truly benefit from a new loan. Some clues that it might be a good idea are: Interest rates are low. Your credit has improved since you got your first loan. You will keep the loan for a long time. You can avoid getting stung by a high-risk mortgage.

How does a refinance work for the appraiser?

The lender makes a few bucks, the appraiser gets a few bucks, the title insurance/closing agent earns a commission, and you save some money. It’s a win-win for everyone but your current mortgage holder, but don’t feel too badly, especially if you gave them a chance to have your refinance business.

Do you have to bring cash to closing for refinance?

Lenders are tricky folks, and sometimes what they do is just add the closing costs to the loan amount. You don’t have to bring cash to closing, but instead of owing $200,000, you find after the refinance that you owe $205,000. Sure, you have a lower rate, but was it worth it? Maybe, maybe not.

When do you pay interest on a refinancing?

That’s because interest is collected in arrears. So at closing, you pay the interest for the first part of the month as part of the payoff amount (it’s usually added onto the loan, like in my case, but you could pay it with cash at closing if you like). You also pay the interest for the second part of the month as part of your closing costs.