Is va a reciprocal state with PA?

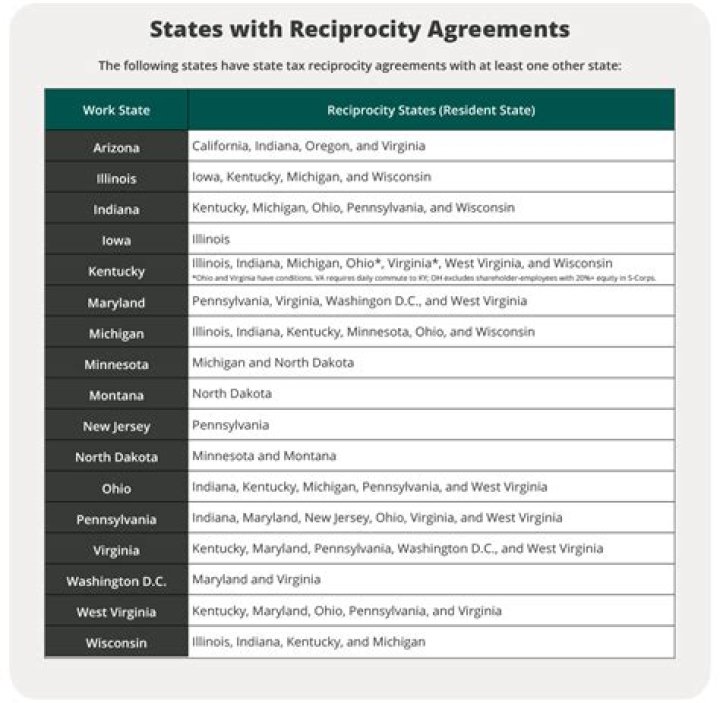

Pennsylvania has signed reciprocal agreements with Indiana, Maryland, New Jersey, Ohio, Virginia, and West Virginia under which one state will not tax employee compensation, subject to employer withholding of the other state. Under the reciprocal agreement, the other state cannot tax the compensation you earned there.

The following states have reciprocity agreements with Pennsylvania: Indiana, Maryland, New Jersey, Ohio, Virginia, West Virginia.

How do I know if I am exempt from Virginia withholding?

If you do not agree to withhold additional tax, the employee may need to make estimated tax payments. An employee is exempt from Virginia withholding if he or she meets any of the conditions listed on Form VA-4 or VA-4P. The employee must file a new certificate each year to certify the exemption.

What happens if you work in Pennsylvania and live in another state?

If you live in Pennsylvania and work in one of the two nonreciprocal states, the Pennsylvania credit is limited to the lesser of the tax you paid to the nonresident state or the Pennsylvania tax due on the compensation that was taxed in the nonresident state.

What happens if you work in Maryland but live in West Virginia?

Let’s say you work in Maryland but live in West Virginia. Thanks to reciprocal agreements, you would pay your taxes to West Virginia where you live. Now let’s say you move to Pennsylvania but keep your job in Maryland. Because Pennsylvania and Maryland also have a reciprocity agreement, you would now pay your tax to Pennsylvania.

What to do when you work in New Jersey and live in Pennsylvania?

For example, a Pennsylvania resident working in New Jersey will give the New Jersey employer a Form NJ-165, Employee’s Certificate of Nonresidency in New Jersey, which certifies the employee is a resident of Pennsylvania and that Pennsylvania’s income tax should be withheld rather than New Jersey’s income tax.

Do you have to live in Maryland to pay Virginia tax?

Maryland, Pennsylvania, or West Virginia Residents who: Are taxed in your home state, and Are present in Virginia for 183 days or less during the year, and Do not maintain an abode, such as a house or apartment, in Virginia, and Receive only wage or salary income in Virginia.