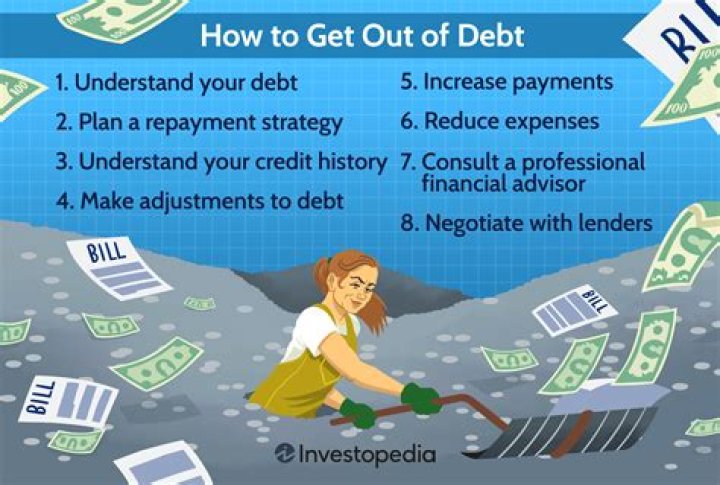

Should I take money out of my investment account to pay off debt?

Investing and paying down debt are both good uses for any spare cash you might have. Investing makes sense if you can earn more on your investments than your debts are costing you in terms of interest. Paying off high-interest debt is likely to provide a better return on your money than almost any investment.

Is it bad to pay off credit lump sum?

Never make a lump-sum credit card payment The interest rate you pay on your credit card debt could be higher than the interest on your mortgage, student loans and auto loans – combined. Each day you don’t make a payment means more interest accrues on your debt balance.

Does amount paid off affect credit score?

Paying off a credit card doesn’t usually hurt your credit scores—just the opposite, in fact. It can take a month or two for paid-off balances to be reflected in your score, but reducing credit card debt typically results in a score boost eventually, as long as your other credit accounts are in good standing.

When to take money out of investment account?

Your broker can help you determine how many of which investments you’ll need to sell in order to obtain the amount of cash you want. Then you have to wait for a few days for the sale to fully settle before your cash is ready to withdraw.

How can I use my savings to pay off credit card debt?

There are several options. You could use everything but $1,000 to slay the debt. You could put a hefty chunk of your savings toward the debt. You could transfer the debt to a card with a short-term 0% interest rate. You could just redirect all money that was going toward savings, to debt repayment.

Can a credit card company take money from your account?

Under state law, if you are delinquent on ANY account, they are authorized to take money from your accounts to bring the credit card account current. Or worse, to take every dollar you have in those accounts to pay down the balance owed.

Is it better to pay off debt or invest?

Some people’s instinct is just to get all debt off their plate, but you want to make sure you always have ready funds on hand to ride out a financial storm. So the best course is usually somewhere in between: If you need some liquidity, then pay off a large chunk of the debt, and keep the rest for emergencies and investments.