What are considered write offs?

“Tax write-off” is an unofficial term for expenses that you may be able to deduct on your federal income tax return. Although you’ll often see the term used to refer to business expenses, individuals may also be able to “write off” certain deductible expenses to reduce the amount of income they have to pay tax on.

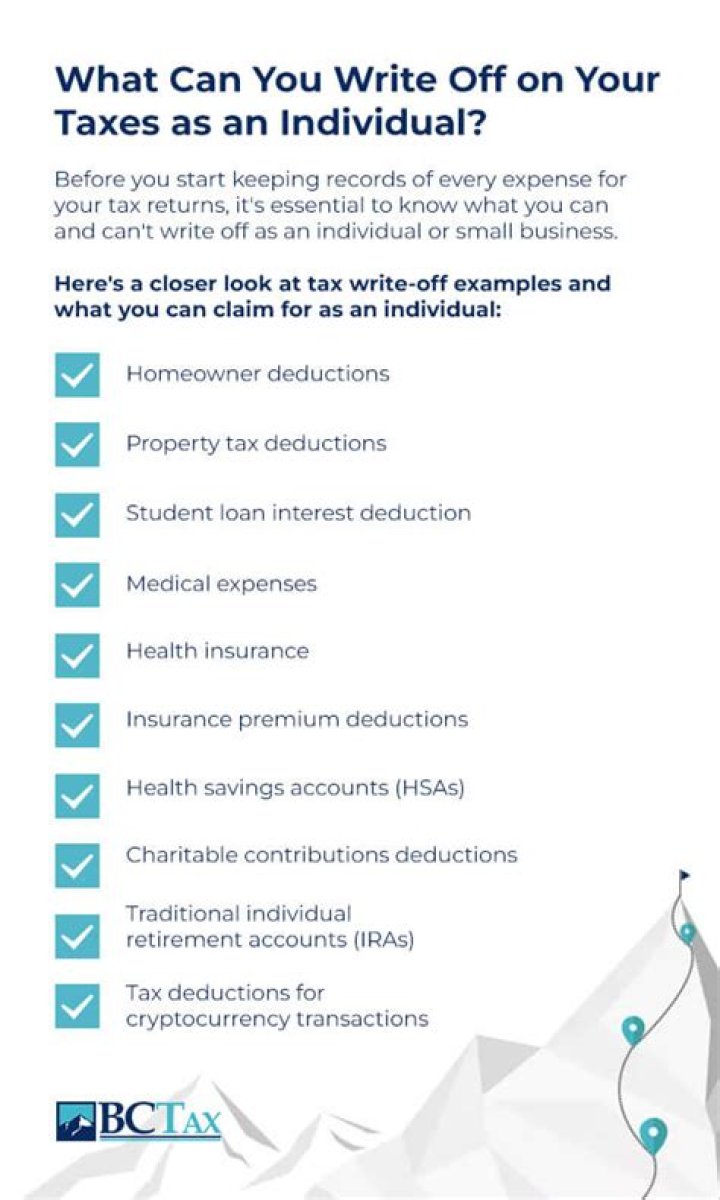

Here are some of the most common deductions that taxpayers itemize every year.

- Property Taxes.

- Mortgage Interest.

- State Taxes Paid.

- Real Estate Expenses.

- Charitable Contributions.

- Medical Expenses.

- Lifetime Learning Credit Education Credits.

- American Opportunity Tax Education Credit.

Which is an example of a write off for a business?

A write-off primarily refers to a business accounting expense reported to account for unreceived payments or losses on assets. Three common scenarios requiring a business write-off include unpaid bank loans, unpaid receivables, and losses on stored inventory.

What are the three most common write off scenarios?

Three of the most common scenarios for business write-offs include unpaid bank loans, unpaid receivables, and losses on stored inventory. Financial institutions use write-off accounts when they have exhausted all methods of collection action.

What’s the difference between a write-off and a loss?

Write-offs may be tracked closely with an institution’s loan loss reserves, which is another type of non-cash account that manages expectations for losses on unpaid debts. Loan loss reserves work as a projection for unpaid debts while write-offs are a final action.

How are write offs reported on the balance sheet?

As such, on the balance sheet, write-offs usually involve a debit to an expense account and a credit to the associated asset account. Each write-off scenario will differ but usually expenses will also be reported on the income statement, deducting from any revenues already reported.