What are examples of deductibles?

The amount you pay for covered health care services before your insurance plan starts to pay. With a $2,000 deductible, for example, you pay the first $2,000 of covered services yourself. After you pay your deductible, you usually pay only a copayment or coinsurance for covered services.

What does it mean when it says deductible?

A deductible is the amount you pay for health care services before your health insurance begins to pay. How it works: If your plan’s deductible is $1,500, you’ll pay 100 percent of eligible health care expenses until the bills total $1,500. After that, you share the cost with your plan by paying coinsurance.

How do I meet my deductible?

Call your insurance company or read your benefits paperwork to verify the deductible you owe. Your deductible will also be listed on your Explanation of Benefits (EOB). You’ll want to meet your deductible early in the year, if possible.

What are common deductibles?

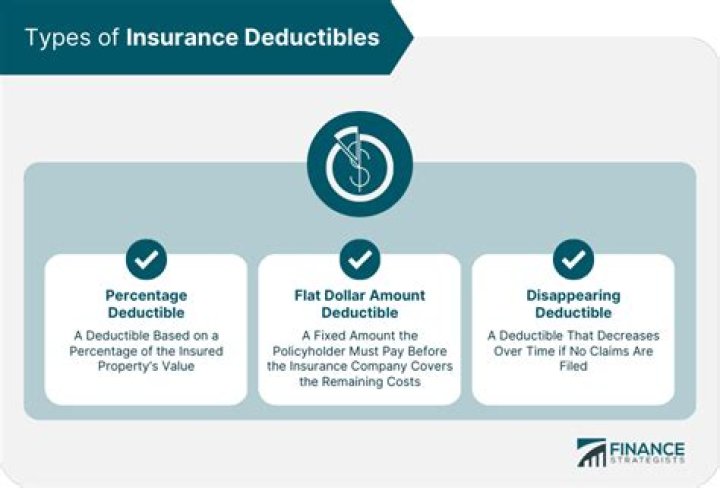

Typically, homeowners choose a $1,000 deductible (for flat deductibles), with $500 and $2,000 also being common amounts. Though those are the most standard deductible amounts selected, you can opt for even higher deductibles to save more on your premium.

What is a $1000 deductible?

A deductible is the amount you pay out of pocket when you make a claim. Deductibles are usually a specific dollar amount, but they can also be a percentage of the total amount of insurance on the policy. For example, if you have a deductible of $1,000 and you have an auto accident that costs $4,000 to repair your car.

What is all perils deductible?

The All Other Peril, or AOP, deductible is usually a flat dollar amount. The AOP deductible applies to covered damages to your property such as lightning, fire, hail, vandalism, and theft to name a few. Each of these claims will be subject to the full amount of the deductible that’s been set.

What are covered perils?

In homeowners insurance, a “covered peril” is an event the insurance company agrees to reimburse you for should you file a claim. Covered perils include fire, lightning strikes, windstorms and hail, weight of snow and ice, theft, and vandalism. Homeowners insurance also spells out which perils are not covered.

Examples of ordinary business deductibles include payroll, utilities, rent, leases, and other operational costs. Additional deductibles include capital expenses, such as depreciating equipment or real estate.

What is a $4000 deductible?

A deductible is the amount of money you pay before your insurance provider begins to pay. This means you pay $1,000 and then the insurance company picks up the tab for the remaining $4,000. If you have a policy with coinsurance you may also be responsible for part of the $4,000 (often 20%).

What do you need to know about deductibles in insurance?

Insurance deductibles are common to property, casualty, and health insurance products. Put simply, they’re out-of-pocket costs that you must pay before your insurance coverage kicks in and pays out your claims. Deductible values vary based on the coverage, insurer, and how much you pay in premiums.

When to tell patients that they have deductibles?

Even practices should communicate it when they are confirming the visit and stay safe from any inappropriate situation. On patient arrival, verify their eligibility and if there are deductibles, share the details with the patients. Make this tip a rule to ensure the financial health of your practice.

What is the meaning of the word deductible?

deductible | American Dictionary. deductible. noun [ C ] us. Your browser doesn’t support HTML5 audio. / dɪˈdʌk·tə·bəl /. an amount of money that you are responsible for paying before your insurance (= protection against loss) will pay you for an expense: Judy’s car insurance policy had a $500 deductible. deductible.

What’s the difference between deductible and out of pocket?

Deductible: How much you have to spend for covered health services before your insurance company pays anything (except free preventive services) Out-of-pocket maximum: The most you have to spend for covered services in a year. After you reach this amount, the insurance company pays 100% for covered services.