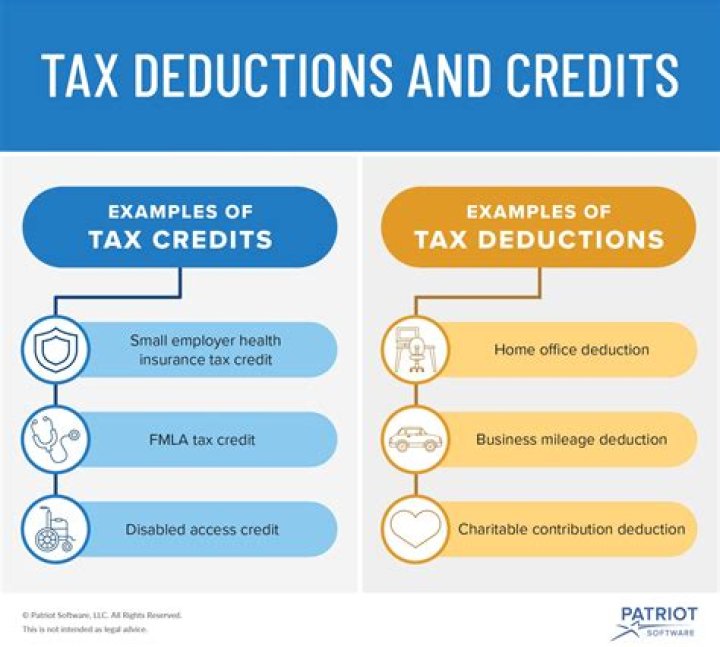

What are tax credits and tax deductions?

Tax credits directly reduce the amount of tax you owe, giving you a dollar-for-dollar reduction of your tax liability. A tax credit valued at $1,000, for instance, lowers your tax bill by the corresponding $1,000. Tax deductions, on the other hand, reduce how much of your income is subject to taxes.

Can you use tax credits and deductions?

How Credits and Deductions Work. Tax credits and deductions can change the amount of tax you owe so you pay less. Credits can reduce the amount of tax you owe. Deductions can reduce the amount of your income before you calculate the tax you owe.

Is a tax deduction better than a tax credit?

Tax credits are generally considered to be better than tax deductions because they directly reduce the amount of tax you owe. The effect of a tax deduction on your tax liability depends on your marginal tax bracket.

Are tax credits or deductions more valuable?

A tax credit reduces your tax liability dollar for dollar whereas a tax deduction reduces the amount of your taxable income – which is used to calculate your tax liability. Tax credits are generally more valuable because they reduce your tax liability by one dollar for every dollar of the credit.

A deduction can only lower your taxable income and the tax rate that is used to calculate your tax. This can result in a larger refund of your withholding. A credit reduces your tax giving you a larger refund of your withholding, but certain tax credits can give you a refund even if you have no withholding.

When to claim tax credits and deductions?

We’re reviewing the tax provisions of the American Rescue Plan Act of 2021, signed into law on March 11, 2021. You can claim credits and deductions when you file your tax return. Tax credits and deductions can change the amount of tax you owe so you pay less. Credits can reduce the amount of tax you owe.

What kind of deductions can I claim on my taxes?

It is allowed as deduction when shares/units/commodities are held as stock-in trade. A public financial institution can claim deduction for its contribution to notified credit guarantee trust for small industries (i.e. Credit Guarantee Fund Trust for Micro and Small Enterprises).

What’s the difference between a tax credit and standard deduction?

With a tax credit, you get it no matter what. No decision required. With a tax deduction, you only get it if you itemize your deductions. When you file your taxes, you can always claim a standard deduction. The standard deduction is meant as a catch-all and you don’t have to do anything extra to get it – everyone can take it.

What are the different types of tax credits?

There are two types of tax credits: A nonrefundable tax credit means you get a refund only up to the amount you owe. A refundable tax credit means you get a refund, even if it’s more than what you owe.