What are the tax implications of a revocable trust?

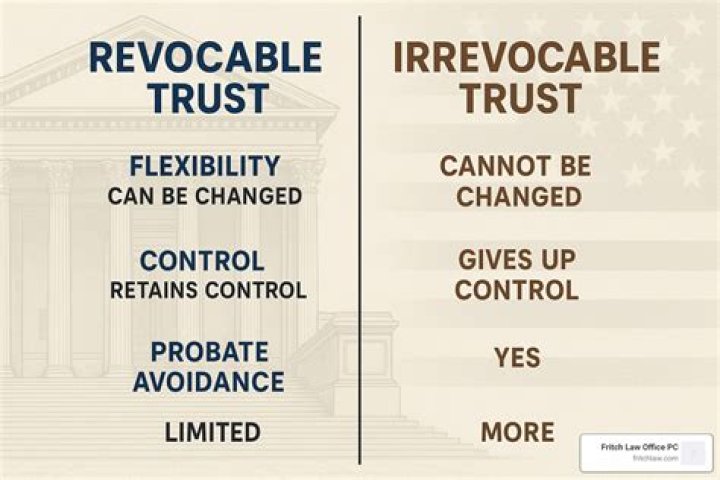

Revocable trusts are not subject to gift taxes, but will be included in the grantor’s estate for estate tax purposes. Estate tax savings provisions can be included in a Living Trust, but a Living Trust has no more estate tax savings potential than a traditional Will.

Is revocable trust income taxable to beneficiary?

When trust beneficiaries receive distributions from the trust’s principal balance, they do not have to pay taxes on the distribution. The trust must pay taxes on any interest income it holds and does not distribute past year-end. Interest income the trust distributes is taxable to the beneficiary who receives it.

Revocable trusts are the simplest of all trust arrangements from an income tax standpoint. Any income generated by a revocable trust is taxable to the trust’s creator (who is often also referred to as a settlor, trustor, or grantor) during the trust creator’s lifetime.

Does estate planning reduce taxes?

For over 100 years, the United States Federal Government has taxed a person’s assets that remain after they pass away. However, the current estate planning laws give individual’s an exemption limit that allows them to pass a portion of their assets down to their heirs tax-free.

What are the tax goals of estate planning?

A basic goal of estate tax planning is to transfer as much of your property with as little taxation as possible. One way to do this is to give money away during your lifetime.

How does a revocable trust work in estate planning?

It then dictates the basis for a distribution scheme that can continue well into the future for subsequent named beneficiaries. All property in a revocable trust bypasses probate at the death of the grantor. This can be a huge saving in both time and expense. Any property passing through a probate estate becomes part of the public record.

Can a will and testament be used to pay estate tax?

If you have an estate plan, then your Last Will and Testament or Revocable Living Trust will contain specific instructions about which assets should be used for paying the estate tax bill. The typical instructions will state the following:

Can a beneficiary withdraw from a revocable trust?

To provide creditor protection the subsequent beneficiary may not have unrestricted rights to withdraw the principal of the trust, however they can have the right to income and additional support necessary for their “health, education, maintenance and support” according to an “ascertainable standard”.

Can a surviving spouse pay the estate tax?

Property passing outright to a surviving spouse or through a Marital Trust and qualified retirement plans won’t be used to pay the tax unless all other assets have been used first. What does this typical language mean? Here are some examples: Assume that your taxable estate is valued at $4,000,000, and your state doesn’t assess an estate tax.