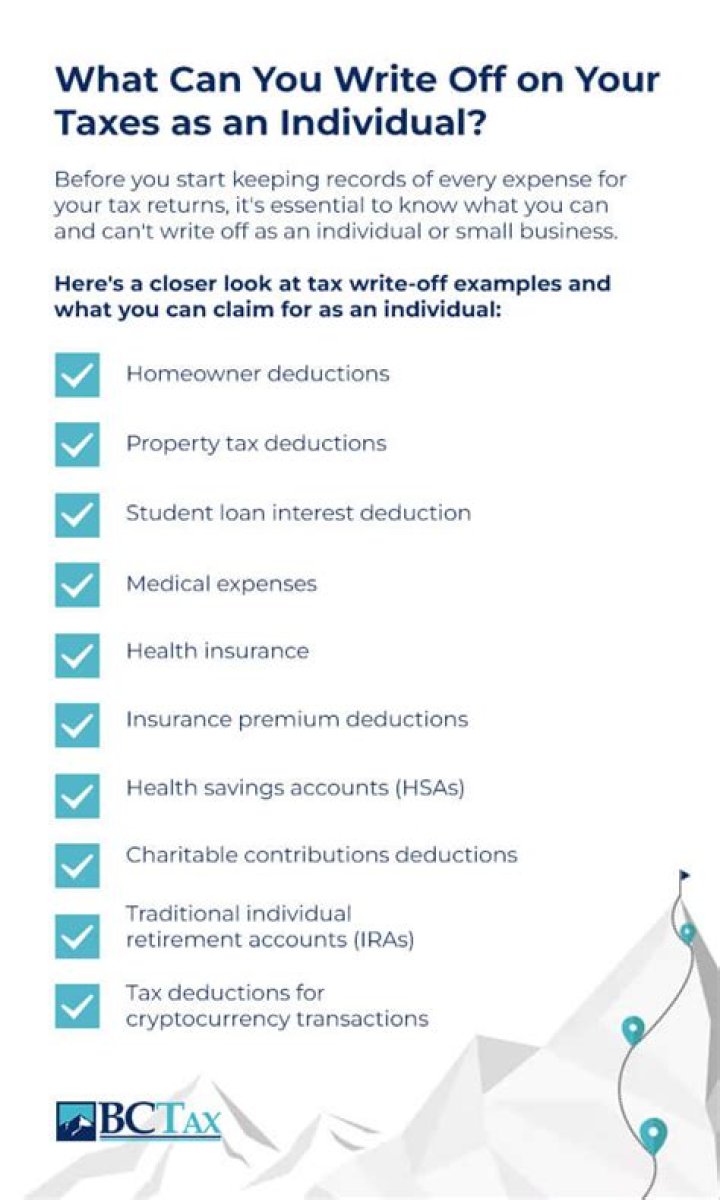

What can you legally write-off on your taxes?

Here are some tax deductions that you shouldn’t overlook.

- Sales taxes. You have the option of deducting sales taxes or state income taxes off your federal income tax.

- Health insurance premiums.

- Tax savings for teacher.

- Charitable gifts.

- Paying the babysitter.

- Lifetime learning.

- Unusual business expenses.

- Looking for work.

How do I write-off bad debt?

Direct write off method. The seller can charge the amount of an invoice to the bad debt expense account when it is certain that the invoice will not be paid. The journal entry is a debit to the bad debt expense account and a credit to the accounts receivable account.

Can a tax deduction be made for a write off?

Such a decision by the taxpayer is not regarded as a valid business or commercial consideration. The amount written-off should not be allowed a deduction as the decision is made for reasons other than in the ordinary course of business and on the basis of considerations other than the likelihood of recovery.

Can you deduct qualified contributions on your taxes?

Qualified contributions are not subject to this limitation. Individuals may deduct qualified contributions of up to 100 percent of their adjusted gross income. A corporation may deduct qualified contributions of up to 25 percent of its taxable income. Contributions that exceed that amount can carry over to the next tax year.

How are trade debts written off for tax purposes?

2 1 Writing-Off Bad Debts Bad debts are written-off in a particular year in relation to trade debts which can be proved, by the taxpayer, to be irrecoverable. Trade debts written-off as bad are generally allowable as deduction against gross income in computing adjusted income.

What do you write off as loss carryover on taxes?

Tax Loss Carryovers If your net losses in your taxable investment accounts exceed your net gains for the year, then you will have no reportable income from your security sales. You may then write off up to $3,000 worth of net losses against other forms of income such as wages or taxable dividends and interest for the year.